“Successful traders know that a consistent and systematic review of their daily trading activities is the direct path to growing and improving”

– Van K. Tharp

While looking at the movements of your charts, play the Reflection song by Lea Salonga and sing along with these lines: What is that trade I see? Staring straight, back at me. Why is the reflection something I don’t want?

Reflecting is not only done for the state of your mental health, to have a clear mind, or even to create better decisions. Reflecting must also be done when investing and trading to create sound and correct decisions. In order to do this, you must have a good, healthy, and peaceful environment. At the same time. It is very essential to have your thoughts and actions documents. Just like how you journalize the things you do every day; you must also journalize your investments and trades!

For investors and traders, journalizing helps develop a more efficient and effective strategy in dealing with the market. With journalizing, you can see your mistakes clearly and what were the principles and rules that you have went against. At the same time, you can look at where you have excelled in! That’s the great thing about journalizing, it gives a peace of mind and determines the areas where you need to improve on. It instills the value of sticking with the rules and principles in beating the market.

One thing to know about journalizing your trades and investments is that it develops the discipline and habit of documenting every transaction that you have made — from buying to selling, and even checking the chart movements.

Here are the things you should know when creating a journal for your trades.

Step 1: Determine what stock to purchase and what type of stock

It’s a must to know the stock you will be purchasing. But not only that, you must know what stock you will be purchasing. Is it a speculative stock? Defensive? Cyclical, blue chips, or tech stocks? This initial step already determines if you are a good trader. A good trader knows where he or she invests in. You can use either technical or fundamental analysis, or combination of the two. Remember, the organization of your trades starts on your discipline in analysis.

Step 2: Listing the quantity of shares bought

Do not rely on the information and journal given by your stock brokers. Record and list down the quantity of shares bought so you can be fully informed about your total investment. This will help you note if have already gained or made losses in your portfolio.

Step 3: The buy and sell point

This refers to the entry/exit point at which you decide on the price you would buy or sell your stock. To limit losses, you must note your target profit and stop loss. The benefit and essence of this step is to know the progress or status of your holdings.

Step 4: Type of time holding period

Determine on how long would you be holding the stock. Would it be for 3 weeks? For 2 months or 3 years? Decide whether you would be holding it on a short, medium, or for long term.

Step 5: Trading Strategy

Trading strategies and holding period goes hand on hand. Journal whether you will be strategizing it with position trading, swing trading, day trading or scalping. Being informed with your strategies will help you on your decision making

Step 6: The buy signal and the reason

Journal the signals and indicators at which made you buy a stock. Were you just hyped with the news or alongside with the comments of traders? Always make a logical and clear decision with a good foundation of analysis, not with feelings. This will also help you understand more the importance of understanding the market structure and indicators. Was there a breakout? A hammer candle stick? A double bottom or an ascending triangle?

Step 7: Date when sold

Consider all dates important, as if they were your anniversary or even your birthday! Treat this as an important component of your trade for it will determine if you broke your rules and time frame.

Step 8: The sell signal and the reason

Selling your stock also goes hand on hand with your time frame. Determine what was the reason for selling. Have you reached your stop loss or target profit? Was there a market breakdown or have you foreseen that the market is on downtrend?

Step 9: Principles and Results

As much as every step is important, you would and must also see the results of your trades! Have your stocks been performing well? Have YOU been performing well? Were your imposed rules and principles followed? If not, what were the results of your non-compliance with your principles?

Conclusion

Consider every step important. With the discipline of journaling, you will always continue to grow and develop the areas you need to improve more!

Take note: You do not just record your success but failures as well! TAYOR!

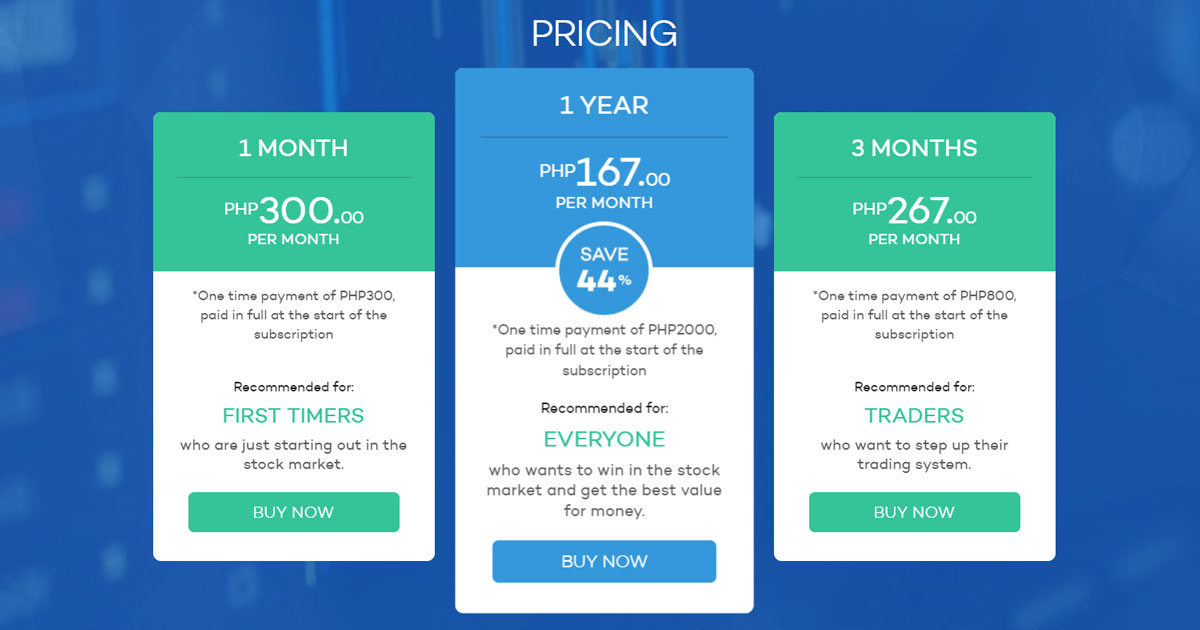

Track your trading performance with InvestaJournal. Now available on InvestaPrime’s FREE 14-DAY TRIAL!

Click on the photo to get your InvestaPrime FREE ACCESS.

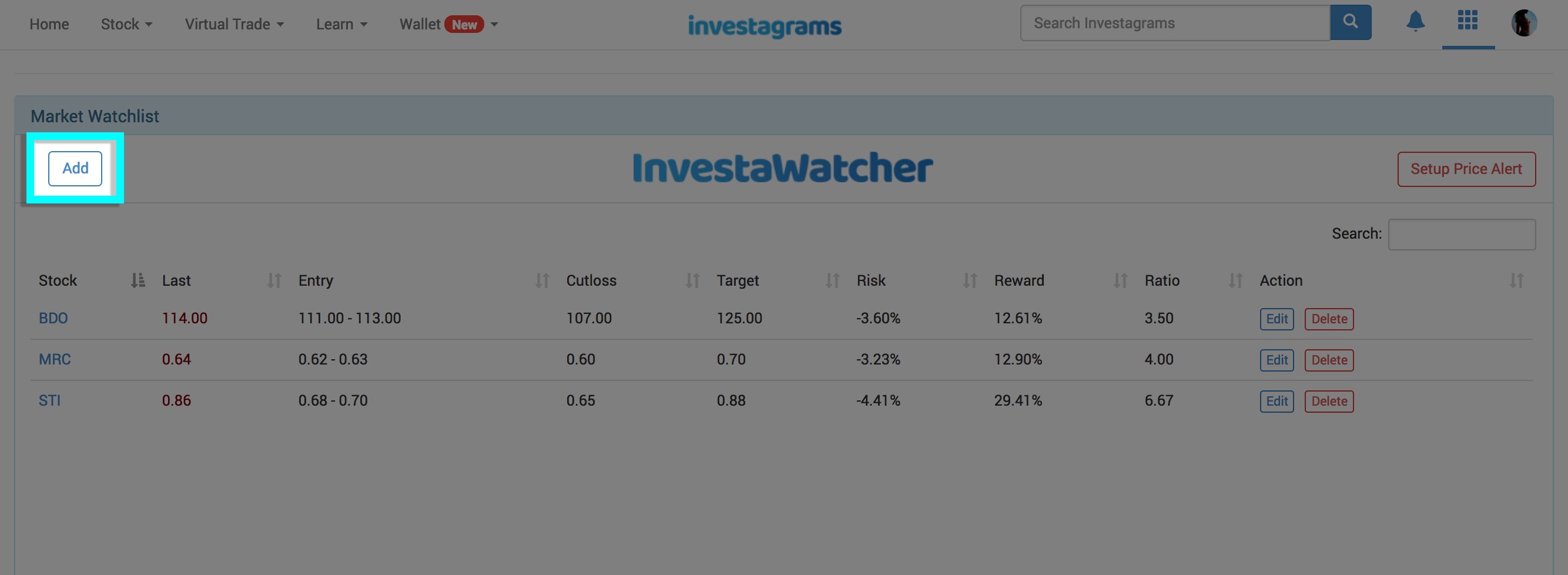

One of the most common reasons why people don’t invest is because they “don’t have time” to monitor the stock market. Well, with InvestaWatcher you can let us watch your stocks for you! Scroll down to see how you can set up your own InvestaWatcher account in just 3 easy steps.

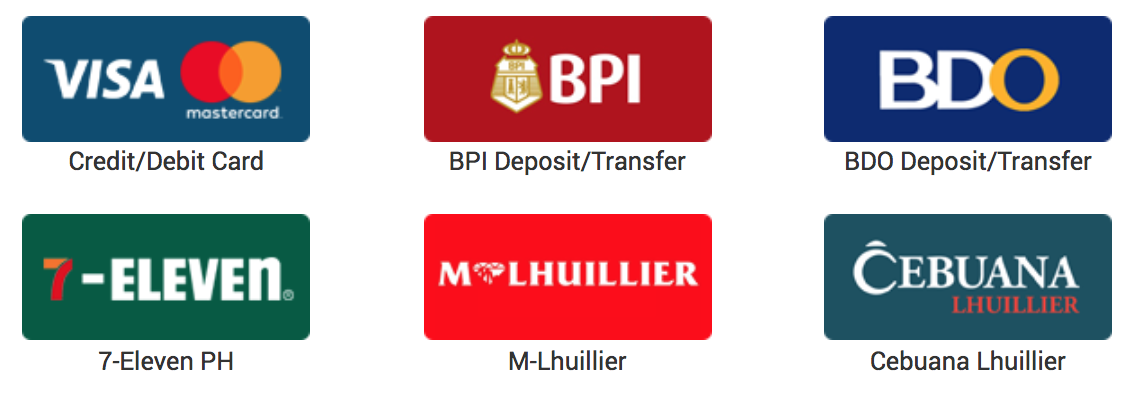

Settle your payment through Debit/Credit Cards, bank transfer to BPI or BDO (deposit or online funds transfer), or at any 7-Eleven, M-Lhuillier or Cebuana Lhuillier branch.

STEP 2: ADD STOCKS TO YOUR WATCHLIST

Once your payment has been confirmed, you can start adding stocks to your watchlist.

Simply go to your Investagrams account and click on the “Watcher” tool on the upper right corner.

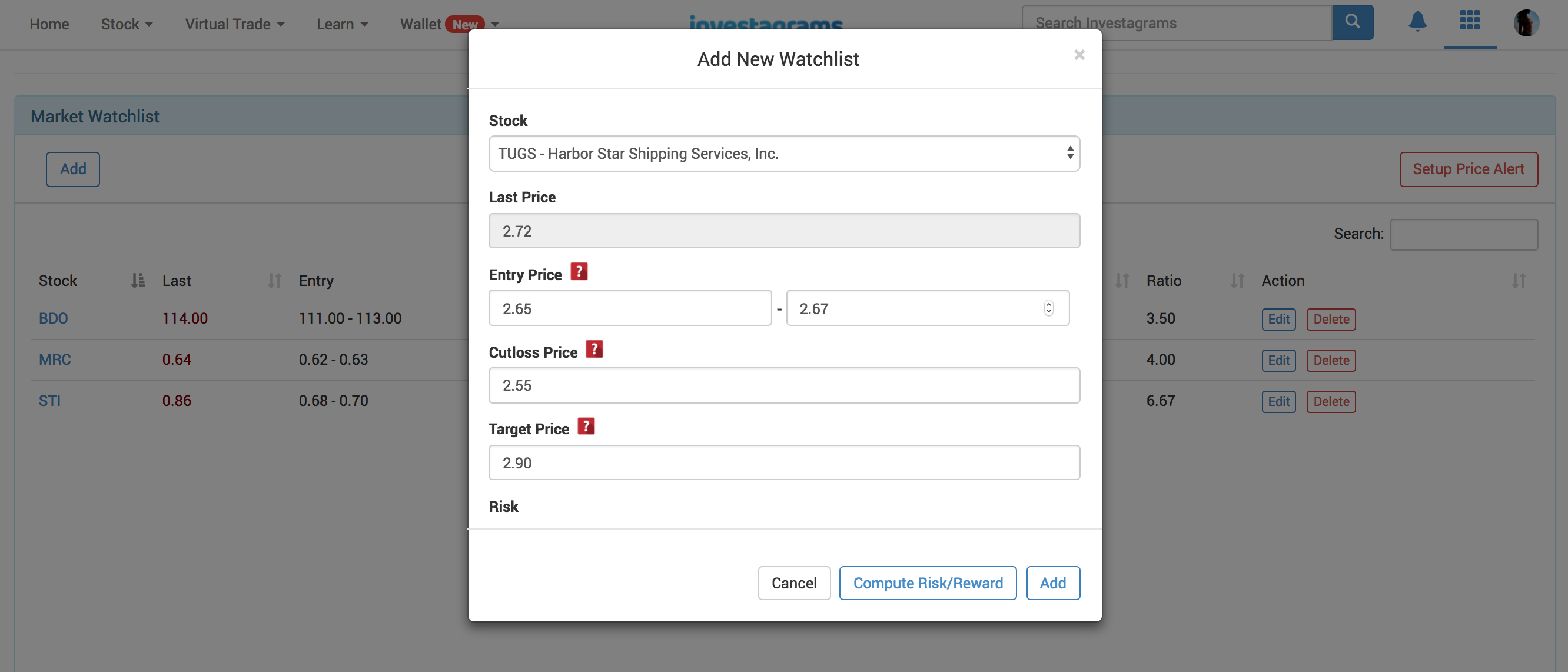

Once you land on the InvestaWatcher page, click “Add” to start adding stocks to your watchlist.

A pop-up will appear for you to input your stock pick, entry, cutloss, and target prices:

Entry Price – The range of prices where you want to buy the stock. You will only receive an alert if the price hits this range. If the price jumps past your defined range, you will not receive an alert.

Cutloss Price – The price where you plan to cut your losses and sell your shares. You will receive an alert if the price reaches or falls below the number you enter.

Target Price – The price where you plan to sell your shares and realize your profit. You will receive an alert if the price reaches or goes higher than the number you enter.

Once you’ve entered all the information, click the “Add” button on the lower right of the box to finish setting up your stock.

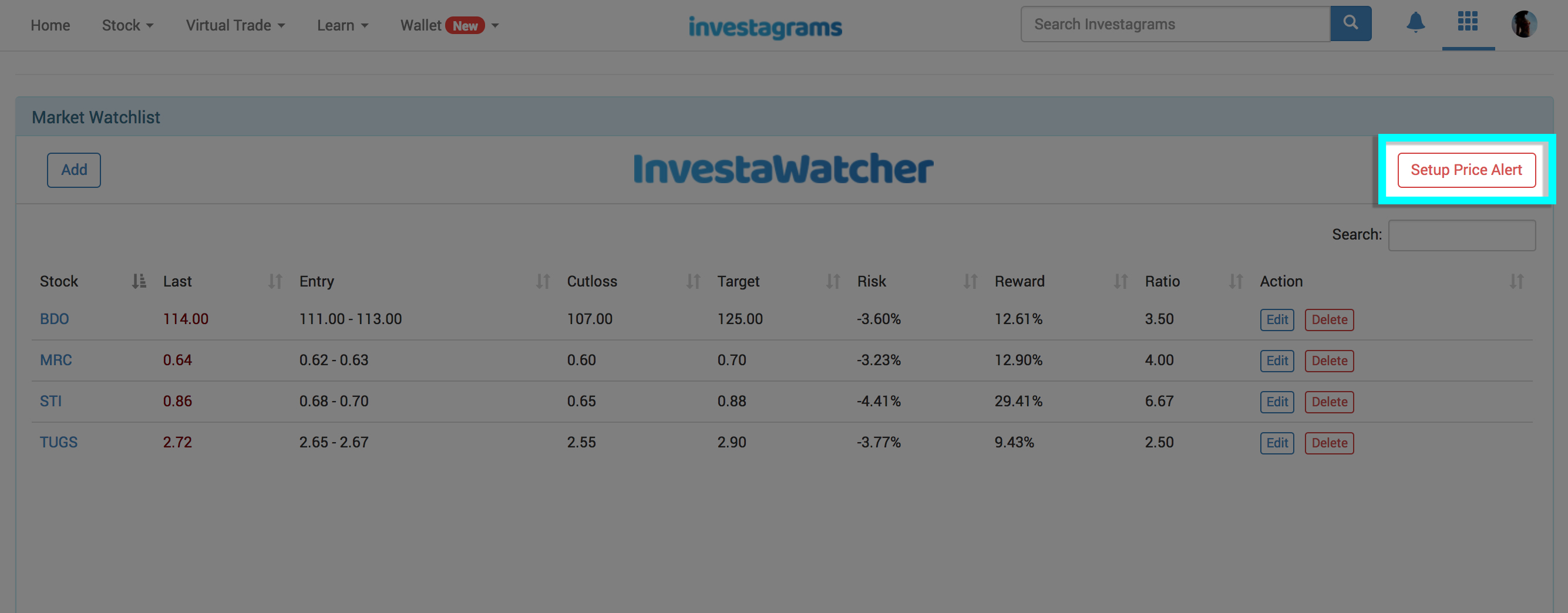

Repeat this for all stocks you want to add to your watchlist. You can add up to 15 stocks.

STEP 3: CHOOSE HOW YOU GET YOUR ALERTS

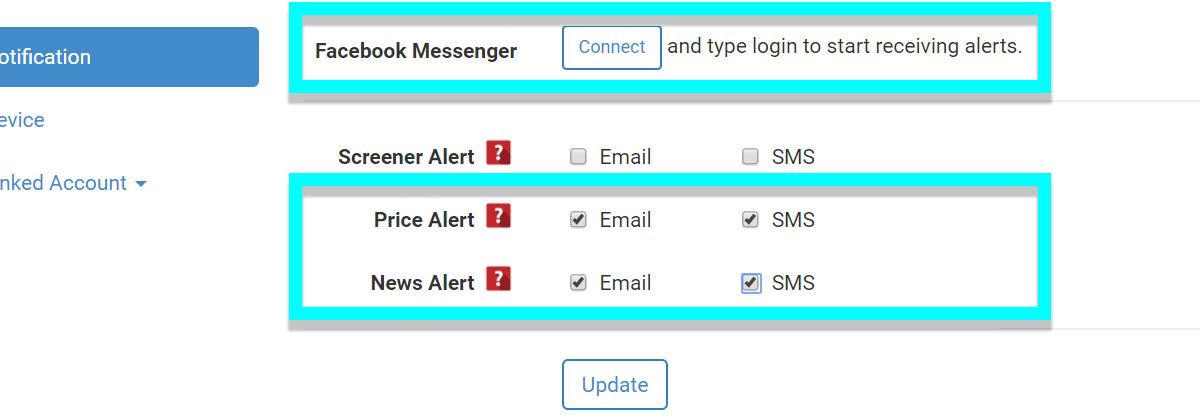

To customize how you get your alerts, just click on “Setup Price Alert” on the upper right corner of your InvestaWatcher page.

You will be taken to the settings page where you can choose which information you want to receive alerts on—price alerts only, news alerts only, or both. You can also turn alerts on or off for SMS, Facebook Messenger, and email.

That’s it! Now you can sit back and relax as we watch your stocks for you. Easy, right?

Not yet subscribed to InvestaWatcher? Click here to learn more and start hassle-free trading now!

Support and resistance may be one of the most basic concepts in stock trading and technical analysis, but it is also one of the most useful. If you know how to use them well, you can already start building a profitable trading strategy. So here are 3 simple but powerful ways to use support and resistance in making profitable trades.

1. Find the best time to buy or sell your stocks.

This is a very basic use of support and resistance, but it is still one of the most effective.

The support and resistance levels often serve as an indicator of a coming shift or reversal of the current price movement. These levels serve as a guide for when we should start buying or selling a certain stock.

We buy stocks as the price nears the support level. Once it reaches the support, demand becomes stronger than supply and more people will want to buy that stock, making the price go up.

On the other hand, we sell stocks as the price gets closer to the resistance levels because this is when you can sell for the highest price. When the stock reaches the resistance level, more people will want to sell and the stock price will start going down again.

2. Identify stronger support and resistance by the length of time.

There are many support and resistance levels that can be found in a chart based on how long or short the time frame is. The longer the time frame, the stronger the support and resistance and the harder they are to break. In other words, a 10-year support or resistance is much stronger than a 1-month support or resistance.

Although the interpretation of a chart is subjective and different for everyone, seeing the bigger picture gives traders an idea of where the stock can go and how easy or difficult it will be for the stock to get there.

Next time you’re looking at support and resistance, try looking at the support and resistance across different time frames to see what the big picture really looks like.

3. Spot potential breakouts, which can lead to huge profits.

The resistance level, once broken, becomes the new support level. If sustained, it gives traders an idea that there is very strong demand for the stock. Breakouts like this usually signal the start of a major price trend, which can lead to huge profits.

This increased volatility during breakouts attract traders because it can offer great returns with a minimal amount of risk, especially if there is no existing resistance in place (i.e. when a stock breaks out to a new all time high).

Keep an eye out for breakouts and wait to see if they are sustained. If they are, it’s likely that you’ll be able to make a profit off of buying that stock.

Don’t forget, you can also combine these concepts to make your trading decisions.

For example, if you see that a stock has broken above its 10-year resistance, then you know from #2 and #3 above that it has the potential for huge profits and you should definitely consider buying that stock. If you want to buy a stock but it’s near its resistance level, then maybe wait a few days to get a better price.

Simple moves like this, applied consistently and with proper risk management will help you become a more profitable trader.

Do you have other tips and tricks for using support and resistance? Let us know in the comments below!

A lot of people ask us, “What is the best investment for beginners?” or “Saang investment ba yung ok?” There are so many options these days that it’s hard to figure out the difference between them all.

So how do you find the best investment for you? It all starts with getting to know yourself. Parang love lang yan. You can’t find your perfect match if you don’t know who you are and what you want. (What you really, really want.)

A lot of people would just say, “But I know what I want. I want to make as much money as possible!” Well, that’s the catch isn’t it? Do you know what’s possible given your current situation? Every person has different resources and abilities, so here are some questions you need to answer first before deciding where to invest:

1. How much money can you invest?

As the saying goes, you need money to make money. Each peso you invest is like a seed—the more seeds you have, the more trees you can grow, and the more fruits you can harvest. The more money you have to invest, the more money you can aim to make.

The amount of money you can invest will also determine which investment options are available to you. Investing is not only for the rich, but there are some investments that require a lot of capital.

A good rule of thumb to find out how much you can invest is to subtract 6 months worth of expenses from your savings. The remaining amount is what you can invest.

Total Savings – 6 Months of Expenses = Investment Fund

Every month, make sure you still have enough money to cover 6 months worth of living expenses before adding more money to your investment fund.

It’s important to keep your investment fund separate from your living expenses because investing is not a get-rich-quick scheme. It takes time. If you need to pull out your investment too soon, then you’ll likely end up losing money—and nobody wants that.

2. How long can you keep your money invested?

Aside from money, another very important resource when investing is time. The longer you’re willing to keep the money invested, the more investment options you’ll have and the more money you can potentially make.

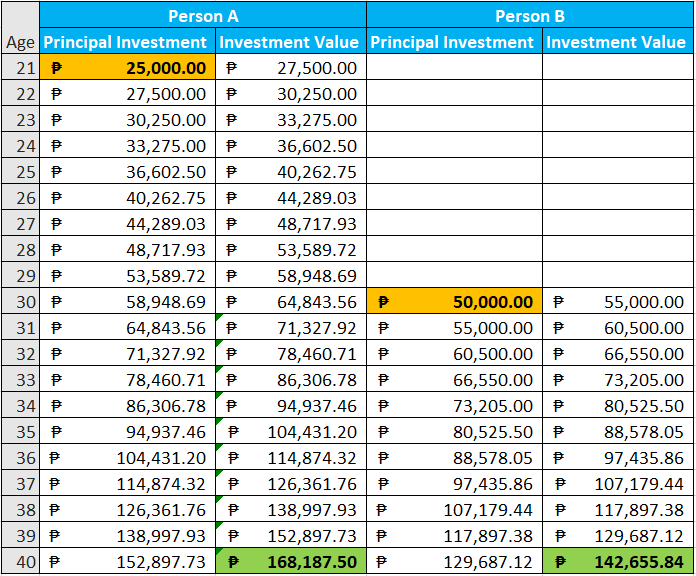

Because of compounding interest, your money will grow exponentially faster every year you keep it invested. As the interest from your investment is added to the next year’s principal amount, the impact of compounding interest becomes so big that the amount of time eventually outweighs the amount money you invest.

Here’s an example showing two investors, Person A and Person B. Person A invested P25,000 when he was 21 while Person B invested P50,000 when he was 30. Assuming the interest rate is always 10% for both cases, you’ll see that Person A’s investment will actually be worth more when they’re both 40 years old—even though Person B put in twice as much money.

When investing, think long-term. You’ll get the best results if you can invest your money for 10 years or more.

3. How much effort can you put into managing your investment?

If you have the time and dedication to educate yourself and manage your own investment, then you can save a lot on fees that would normally be paid to fund managers and financial advisers. It may even open up some investment opportunities that you couldn’t consider otherwise.

For example, a lot of people nowadays are marketing small businesses as investments—food carts and farming are just two examples. People will automatically ask “Ok ba ito?” and someone who has done it before might say “Oo! Laki ng return ko diyan!”

While it’s true that businesses can be great investments, they will only succeed if you put in the time and effort to run it well. Otherwise, you’ll just be throwing your money down the drain.

If you don’t have the time and energy to manage a high-maintenance investment, don’t worry. There are a lot of other investment options out there, which we’ll discuss later.

4. How much risk are you willing to take?

By now you’re probably tired of hearing this over and over, but it’s true—if you want bigger rewards, you’ll need to take on bigger risks. It’s difficult is to figure out exactly how much risk is right for you, but one thing’s for sure: There is no risk-free investment.

If you’re putting your money somewhere that’s risk-free, the interest rate will be so low that you end up losing money due to inflation. And if you’re losing money, then that’s not really an investment anymore.

Take savings accounts for example: Banks guarantee to keep your money safe and you definitely won’t lose a single centavo. However, the interest rate for most savings accounts is only 0.25%. That’s around 2.75% less than the average inflation rate, meaning that the value of your money decreases by 2.75% every year!

On the other hand, investing all your money in a new company that may or may not exist next year could lead you to lose all your money. But you might also have invested in the next Facebook and end up making a bigger profit than you ever dreamed of.

It’s always a balancing act when we talk about risk and reward, and the perfect mix is different for everyone. You need to take some time and really think about what would be the right balance for you.

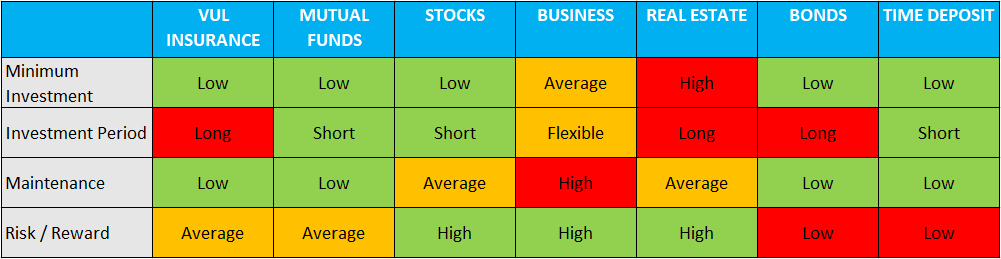

Main Investment Options in the Philippines

Here’s a table summarizing the main investments available in the Philippines, and what their characteristics are in relation to the four questions above.

If you find any of these interesting, then scroll down for more details.

VUL Insurance

VUL insurance plans are one of the most popular investment options in the Philippines. It’s a flexible and low-maintenance investment that hits three birds with one stone—life insurance, health insurance, and mutual funds. If you don’t have insurance yet, you should seriously consider getting VUL insurance.

Minimum Investment: VUL insurance plans are very flexible because they are personalized to your needs. You can have premiums that are as low as a couple thousand pesos per month. Just keep in mind that your benefits will be proportionate to the amount you invest.

Investment Period: Though there is some flexibility with VUL insurance, it’s best to aim for an investment period of at least 10 years. Most plans will deduct the largest fees in the first few years and let you invest for free by the 5th year or so.

Risk and Return: The risk profile and rate of return with VUL insurance is average overall, but can be adjusted based on your preference. Insurance companies usually have a few funds that cater to different risk profiles. Just make sure to get a good insurance agent so they can customize the best plan for you.

Recommended For: First-time investors who want an all-in-one package and don’t mind a long-term commitment

Mutual Funds

Mutual funds are another low-maintenance investment that is popular among Filipinos and especially working professionals. It has a lot of the same benefits as VUL insurance, but with two key differences: you won’t get any insurance (obviously) and you can think relatively more short-term. Put simply, mutual funds operate by pooling together money from many different investors and investing those in various assets and securities. That way it’s easier to diversify and manage risk.

Minimum Investment: Some mutual funds in the Philippines now have minimum investments as low as P5,000. The minimum investment will vary depending on which fund you’re looking at, but they’re all relatively low as far as investments go.

Investment Period: There is usually a lock-in period for mutual funds, though they can be as short as 90 days. You could even take out your investment earlier if you need to, but there will be a penalty. And of course as with any investment, you should think long-term if you want to see the biggest returns.

Risk and Return: Similar to VUL insurance, mutual funds have an average amount of risk and return. They can be higher or lower depending on the exact fund you choose, but professionally managed funds will be less risky than managing your own money.

Recommended For: Busy bees who just want to put their money somewhere where it can grow

Stocks

If you’re after bigger returns and don’t mind taking on a little more risk, then investing in stocks is a great way to go. It’s like the DIY counterpart to mutual funds. You’ll have to put more time and effort into managing your investment, but you’ll also have greater potential returns because you won’t have to pay any fund management fees.

Minimum Investment: Nowadays, you can open a stock trading account for as little as P2,500. Some brokerss won’t even require a minimum investment if you already have a savings account with their bank. Just keep in mind that, if you can afford it, we would still recommend start with at least P8,000. More on that here.

Investment Period: Stocks are very liquid investments, which means that it’s easy to sell, take your cash, and get out at any time. But keep in mind that even stocks require some time to earn substantial returns. There’s also a good chance that you will lose money if you need cash and have to sell your stocks at a loss. Always remember: Investments are not get-rich-quick schemes.

Risk and Return: Directly investing in stocks as an individual does carry more risk than VUL and mutual funds. Unlike professional fund managers, you won’t have a big corporation and fellow professionals helping you out. You’ll also have a smaller fund, which means you won’t be able to diversify your stock picks and manage risk as easily. Of course, the upside to all of this is that if you succeed, you’ll get to keep all the profits for yourself.

Recommended For: People who want bigger returns and are willing to dedicate time to managing their investment

Businesses

Minimum Investment: The initial investment for businesses varies a lot depending on the type of business you choose. It can be anywhere from a few thousand to a few million pesos. But whatever type of business you’re looking at, just remember that you’ll probably need enough cash to cover more than just the upfront cost. You’ll need to have enough money to cover costs for the first few months when your business may not be earning money yet. Not to mention, you’ll also need to invest a ton of time and effort if you want to give your business the chance to succeed.

Investment Period: It takes time for businesses to break even and earn a profit. While some only take a few months, others can take years. And either way, one thing’s for sure—there is no such thing as an overnight success. You’ll need to work hard and work consistently on building your business if you want any chance of seeing a return on your investment.

Risk and Return: A business is one of the riskiest investments you can make. It takes more work than any other investment, and even then a lot of businesses will fail within the first year of operations. But if you’re willing to take the risk, put in the work, and keep going despite the challenges, then your business could become a cash cow and the best investment you’ve ever made.

Recommended For: Strong-willed and self-motivated risk-takers who will do whatever it takes to succeed

Real Estate

There are two popular types of real estate investments in the Philippines—condos and land. There are some differences depending on which one you choose, but both don’t require that much maintenance and the potential return is quite high. If you can afford the high price tag, real estate might just be the right investment for you.

Minimum Investment: Depending on where the condo or piece of land is located, your cash out can be just a few hundred thousand pesos or a few million pesos. Compared to other options like stocks or mutual funds, you’ll definitely need to spend more money, but it could also pay off greatly.

Investment Period: With real estate, you can make money two ways: by renting out your property or through price appreciation. In both cases, it will take time for you to earn a profit. If you’re renting out a condo, you’ll likely have to hold on to your investment for at least 10 years before you recover your cost and start seeing returns. You could see returns faster if you’ve invested in land, but even this will depend heavily on the location of the land you’ve bought.

Risk and Return: Real estate is a high risk high reward type of investment. The initial cash out is very high compared to other investments, and it’s very difficult to sell if you suddenly need cash. Not to mention that even though the returns can be huge, they are not guaranteed. Investing in land is generally a bit safer than investing in a condo, but the demand for either can be unpredictable. Before investing in any property, make sure you do your research.

Recommended For: Seasoned investors looking to diversify their portfolio of assets and investments

Bonds

If you’re the conservative type of investor and don’t mind a lower rate of return, you can look into buying some bonds. When you buy bonds, you’ll know exactly how long you need to wait and you’ll also be guaranteed a certain rate of return. Just make sure that you can leave the money invested for the entire maturity period, because pulling out the investments early will mean losing money.

Minimum Investment: You can invest in retail treasury bonds (RTBs) for as low as P5,000, though many banks will require larger minimum investments. Because bonds have such low interest rates, then you may want to invest more if you can. That way, you’ll earn more actual pesos in profit.

Investment Period: Bonds will usually have longer investment periods that are a few years long, sometimes more. But the good thing is that you can find out the exact investment period upfront, even before you put out any money. Make sure you ask about the bond’s maturity date and that you won’t need the money before then.

Risk and Return: Both risk and return are very low for bonds, which is why they are recommended for conservative investors. Though your money won’t earn huge amounts of interest, at least you’re not likely to lose any money. At the very least, you’ll get an interest rate that’s higher than what you would get in a savings account.

Recommended For: Conservative and risk-averse investors whose main priority is not to lose money

Time Deposit

Time deposits are very similar to savings deposits, except that there is a specific date of maturity when you can take out your money. Because it’s such a low-risk investment, you can expect low returns as well. However, like bonds, this is another type of investment that will at least get you slightly more returns than a regular savings account.

Minimum Investment: The minimum investment for a time deposit can be as low as P1,000. But keep in mind that banks will usually give you a higher interest rate if you put in a larger investment.

Investment Period: The investment period for time deposits can also be very short—as short as 30 days. But again, keep in mind that banks will usually give you higher interest rates if you agree to a longer investment period.

Risk and Return: Time deposits usually have extremely low risk and extremely low returns. Some of them will have an interest rate that’s only 0.25% before tax—that’s the same as a regular savings account. But if you agree to a longer investment period or invest larger amounts of money then you can get a better interest rate. We recommend looking at other low-risk investment options too so you can decide if this is really the best option for you.

Recommended For: Extremely conservative investors who don’t have access to bonds or just prefer a more flexible low-risk investment

Conclusion

At the end of the day, anything that can make your money grow can be considered an investment. These definitely aren’t all the options, but we hope this helped you understand some of the most popular investments in the Philippines better. Only you can take this information and really look within yourself to find out what the best investment for you will be.

What are some of the best investments you’ve ever made? Let us know in the comments below!

At one point or another, we’ve all wondered “What is the minimum investment needed in the stock market?” or “How much should I save before investing in stocks?”

Ever since online stock brokers became popular, it seems like the minimum required investment keeps getting lower and lower. That’s good, right? Well, not always.

If you’ve tried stock trading or know someone who has, then you also know that it’s hard to make money in stocks.

There are over 200 listed stocks in the PSE, and literally thousands of factors that could affect their prices. It’s hard enough just keeping track of everything, let alone understanding each stock well enough to make money!

We don’t need to make life harder for ourselves—but that’s exactly what happens when you invest less than 8,000 pesos in the stock market.

A TYPICAL SCENARIO

Nowadays, some brokers won’t require a minimum investment. Others have been also lowering the minimum amount required so that more people can start investing.

While it’s great that this lets more Filipinos invest in the stock market, there’s a scenario that often gets first-time investors off guard.

The typical scenario goes like this:

Person A is interested in investing in the stock market. He finds out that the minimum investment is only 5,000 pesos. “Sulit na! Kikita naman ako dito,” he thinks to himself.

Person A invests the minimum amount and picks two stocks “para mas mababa ‘yung risk.” That’s around 2,500 pesos in each stock.

After successfully buying the stocks, Person A checks his portfolio and “HUH?? Bakit loss na kaagad? Di pa gumagalaw ang presyo ah!”

That’s what happens when people don’t realize that there are fees every time you buy or sell a stock.

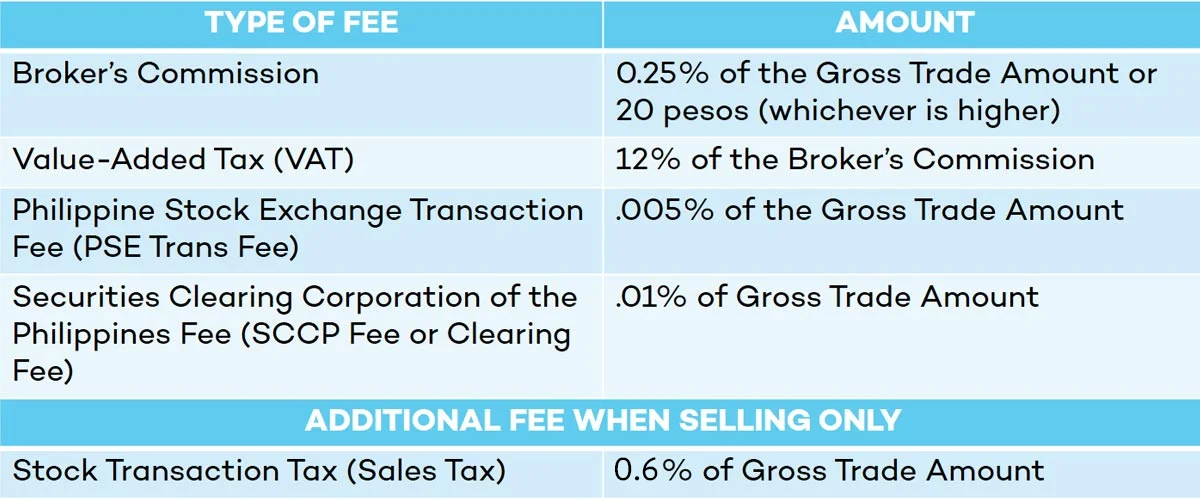

BEWARE OF FEES

Below is a breakdown of all the fees and charges included in every transaction:

Most of the fees are based on the Gross Trade Amount (number of shares x price), so the cost is always proportionate to your investment. For example, the PSE Trans Fee will always be .005% and the SCCP Fee will always be .01%. However, notice that the broker’s commissionis 0.25% or 20 pesos—whichever is higher.

NUMBERS DON’T LIE

So what does this mean for retail traders? It means you need to avoid buying or selling anything with a Gross Trade Amount less than 8,000 pesos. Otherwise, you will be wasting money on higher commission fees and incurring unnecessary losses.

In the example earlier, Person A bought two stocks, each with a Gross Trade Amount of only 2,500 pesos. This means that Person A’s total commission fees would have been 20 pesos for each transaction, or 40 pesos total. That’s an automatic 0.8% loss on commission fees alone!

But what if Person A invested 8,000 pesos in just one stock? His total commission fee would only be 20 pesos (or 0.25% of 8,000). That means he was able to cut the commission fee in half and invest 3,000 pesos more!

CONCLUSION

We know that saving money can be very hard—especially if you have a family to support. 8,000 pesos is a lot of money after all!

But remember that investing less than 8,000 pesos, means you are losing more money even before there’s any price movement. You can definitely still make a profit, but it’s like stepping on the gas and break pedals at the same time. It will be harder to break even or make a profit.

Weigh the risks carefully before making your decision, and ask yourself: How confident am I that the (potential) profits will offset my (definite) losses?

Subscribe to InvestaDaily for more investing tips and stock market advice, or sign up for Investagrams to access special features to help you reach your first million.

In our first video, we taught you the basics of how to read stock charts. We explained candlesticks, trend lines, and support and resistance.

Now, we’ll dive deeper into support and resistance—the backbone of all price structure analysis methods in technical analysis.

Watch the video above to learn how mastering support and resistance can make you a more profitable trader. We’ll also teach you about breakouts, breakdowns, and role reversals—when resistance becomes support or support becomes resistance. This will help you predict the best time to buy and sell.

This video is in a mixture of Filipino and English.

Subscribe to InvestaDaily for more investing tips and stock market advice, or sign up for Investagrams to access special features to help you reach your first million.

Whatever your investing style, knowing how to read stock charts is a skill that is sure to help you succeed in the stock market.

Watch this short tutorial video to learn the basic ways to read a stock chart—including how to read candlesticks, identifying trend lines, finding the support and resistance, and spotting breakouts or breakdowns. All of these will help you understand charts better and make more informed trades.

This video discusses technical analysis concepts in a mixture of Filipino and English.

Subscribe to InvestaDaily for more investing tips and stock market advice, or sign up for Investagrams to access special features to help you reach your first million.