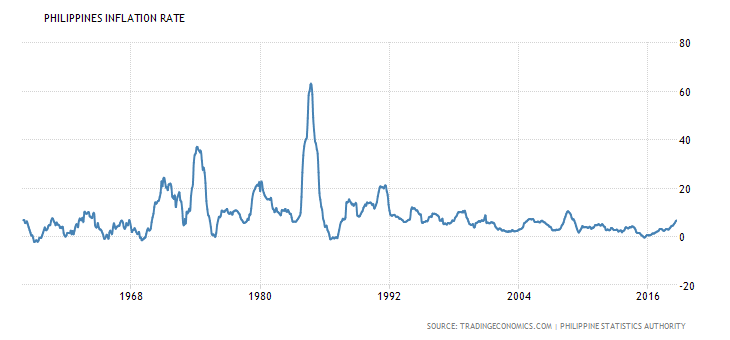

Lahat na ata ng tao alam ang inflation rate dahil kahit saan makikita mo ang issue ng inflation rate dito sa Pilipinas. TV, Newspaper, Social Media (especially Facebook), Office, Schools and etc. Isa to sa mga major issues sa Pilipinas. Bakit nga ba ito naging issue? 6.7% ang current inflation rate ng Philippines (September 2018). Compare to 2.9% of 2017 it is really high. Ngunit ito na ba ang pinakamataas na inflation rate?

If we will compare the 6.4% inflation rate to 60+% inflation rate in late 1980s is it still bad? Diba, hindi na masama? Kung ganyan pa lang ang ating inflation rate as of today, ano pa ang magiging reaction mo kung ikaw yung nasa kalagayan ng mga tao noong 1980s?

Why our inflation rate is high?

Ang inflation rate ay pinaghalong international and domestic factors. Isa sa mga dahilan kung bakit mataas ang ating inflation rate ay dahil na sa “Oil”. Dahil wala tayong sariling production ng oil, lahat ng oil ay import galing sa ibang bansa at dahil din dito Philippines are forced to import oil. Isa pang factor nito ang “Weak Peso”. At dahil sa lahat ng mga import goods ang pinang babayad natin ay foreign currencies mas mataas ang nagiging cost dahil mahina ang peso. Isa sa mga domestic factor ay ang “Bigas”. But not only rice, by the way. Vegetables, Fish, Sugary Foods, and Corns. There are so many effect of the rapidly rising inflation rate so why don’t we start our own investments. Let us learn to have another source of income so our hard-earned money will not be put into waste because of this issue.

What are the effects of inflation rate to different class Filipinos?

It all affects us especially those who are minimum wage earner. Kung may 100 pesos ka ano na lang ang halaga nito? 93.6 pesos to be exact. What if kung ang sweldo mo ay 20,000 per month, ang halaga na lang nito ay 18,720. Sobrang laking bagay nung nawalang pera sayo ng wala naman pinupuntahan. Pare-parehas lang naman ng effect sa mga Filipino pero iba ang nagiging solution ng mga tao. Bakit ba sa bank nag iinvest ang karamihan sa mga Filipino kahit na ang liit liit na ng interest rate? Takot kasi tayo na magtake ng risk, pero hahayaan mo na lang bang talunin ka ng takot mo? Hindi ka magfoforward kung matatakot ka lagi.

Take the risk!

If hindi ka aalis sa comfort zone mo di ka din magfo-forward? For example ang comfort zone mo ay sa loob ng bahay nyo, bakit ka lumalabas? Hindi ka naman kasi mabubuhay kung di ka magwowork.

So instead of blaming the government why don’t you try to do some actions? TRY TO INVEST? TAKE THAT RISK!

If you will not try you will not know. Walang nag umpisa sa stock market ng hindi nalugi or nagkaron ng loss. If you fail wag matakot sumubok ulit but this time different process na or different strategies. Ang mali kasi satin we keep on expecting different outcomes but still doing the same strategies. We even emphasize the issue about the chili pepper or ‘sili’ na nag-viral recently imbes na maghanap tayo ng paraan paano mao-overcome ang ganitong scenario sa bansa.

Hanggang saan ang kailangan kong maging income para hindi ko na mapansin ang inflation rate? Yan dapat ang way of thinking natin. Dahil sa pag-blame mo sa government nauubos na ang oras mo. Why don’t you use your time in learning the stocks market.

“We cannot solve our problems with the same thinking we used when we created them.” ~ Albert Einstein

In failures you will learn so much.

Don’t look at the inflation rate as a burden but instead, use it as you inspiration.

Ilang taon na rin ang nakakalipas simula ng magtrabaho ako after graduation. I was a rising employee sabi nga ng boss ko. Dahil Developer tayo, maraming deadlines kaya laging overtime pero siyempre kasama na din diyan ang pakitang gilas. Bibo tayo dati eh! I sacrificed my life pati yung buhay pamilya ko makamit ko lang yung inaasahang promotion at mataas na sweldo.

Gigising ng maaga tapos magbbyahe ng isa o dalawang oras depende pa yan sa traffic, pero minsan kapag minalas ka, sira pa LRT, o di kaya, pang sampung batch ka na bago ka makasakay. Imbes na fresh ka pupunta sa work, mukha kang nalantang gulay at di naligo ng tatlong araw!

Yan ang mga bagay kung bakit madalas na akong mastress sa trabaho, tapos lagi pang nag-aaya sa labas mga tropa ko. Gastos dito, gastos don. Peer pressure! Paulit-ulit na lang ang cycle ng buhay ko at yung mga dapat sana na inipon ko na lang sa bangko, napunta lang sa wala.

Hindi naman ako mayaman, #feelingrich lang. Akala ko kasi, kapag may sweldo ka buwan buwan at konting ipon sa bangko na minsan eh nababawasan pa, okay na.

Ako ang ‘The Living Legend’ ng rat race story ni Robert Kiyosaki.

Alam mo bang dumating na din ako sa punto na na-experience ang tinatawag ng mga henyo na ‘mid-life crisis’, totoo pala yon. May mga hinahanap ako sa buhay na hindi ko na alam kung ano.

Until one day, I accidentally saw my high school friend somewhere in Pasig and with the usual gesture, napa-kape kami sa Starbucks, ako pa nanlibre. (Yamanin diba?) Nagtanong siya kung malaki daw ba sweldo ko. Ang malupit don, he even asked me “Do you know how to invest? Ang stocks hawak mo ngayon?” Natawa ko e, sabi ko “Bro, kape kape lang tayo, walang networking!” Dahil I have zero knowledge when it comes to investing, sinabi ko sa kanya na baka pang-mayaman lang yon. Well of course, I asked a few questions until that questions became a small training with him about investing in Philippine Stock Market.

I was lucky enough to have a friend na dedicated tumulong at ipaintindi sa kin and mundo ng merkado. He taught me how things work, how to start in investing and how to make my money grow. He also taught me how to open my account sa Investagrams so I could practice trading bago sumabak sa totoong laban. Para akong binuhusan ng malamig na tubig dahil sa edad kong to, ngayon ko lang nalaman ang ganitong mga bagay at nagkainteres kung pano i-value ang hard-earned salary ko.

Fast forward today, nagkaron na ng meaning ang buhay ko (Naks, parang Hows of Us moment lang nila Kathniel!). Malaking pagbabago ang nangyari, nabawasan na ang after-work parties, I allocated time to study more about investing in stock market at madalas ko na uli makasama ang pamilya ko. I’m no longer living paycheck to paycheck, and instead of splurging everything, kasama na sa budget ko ang savings and investment.

‘Pay yourself first’ – a cardinal rule to discipline yourself towards your future goals and financial freedom.

Develop the skills and the right mindset necessary.

Yan lang ang dapat mo gawin at paulit ulit na panghawakan, sabi nga nila, don’t give up. Change how you think and you’ll change the results.

Naka-relate ka ba? Kung oo, I hope my story could help to open your eyes and treat this as perfect time to change. Hindi naman mahirap mag-invest, dedikasyon at yung WHYs mo lang ang kailangan mo to shift your mindset and improve your life for the better.

Salamat sa pakikinig kaibigan,

Your Ka-Investa, #AnonymousInvestaTrader

One of the most common reasons why people don’t invest is because they “don’t have time” to monitor the stock market. Well, with InvestaWatcher you can let us watch your stocks for you! Scroll down to see how you can set up your own InvestaWatcher account in just 3 easy steps.

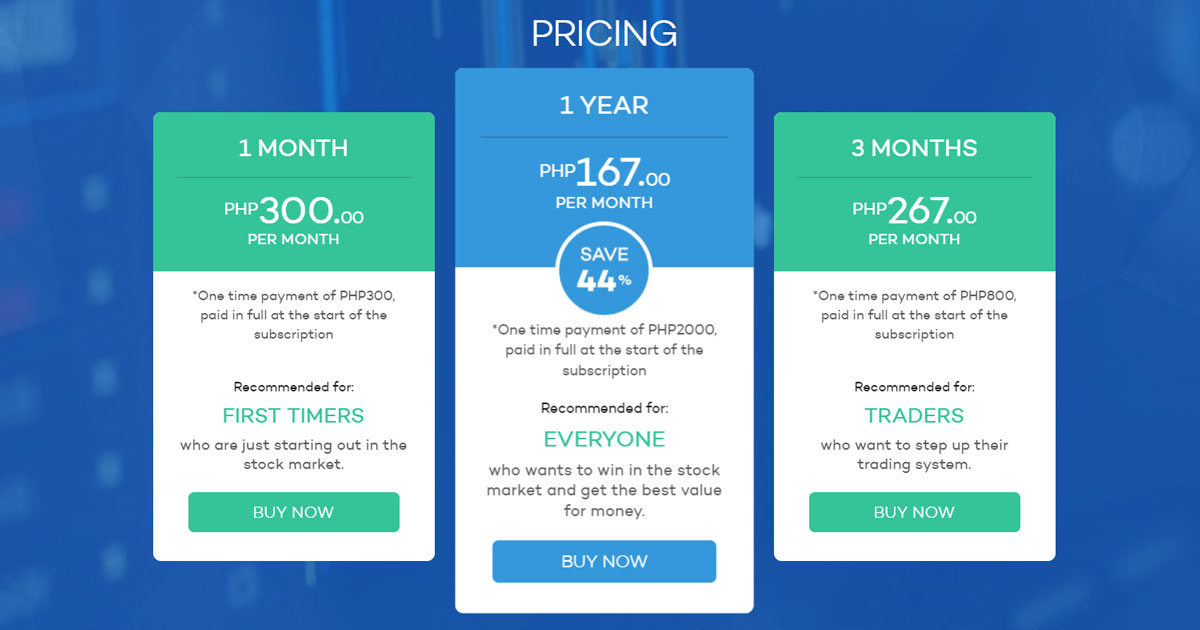

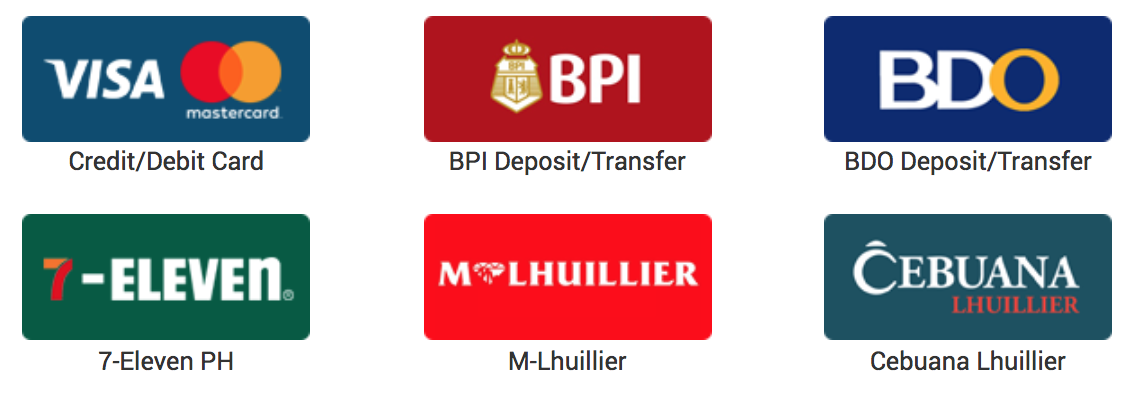

Settle your payment through Debit/Credit Cards, bank transfer to BPI or BDO (deposit or online funds transfer), or at any 7-Eleven, M-Lhuillier or Cebuana Lhuillier branch.

STEP 2: ADD STOCKS TO YOUR WATCHLIST

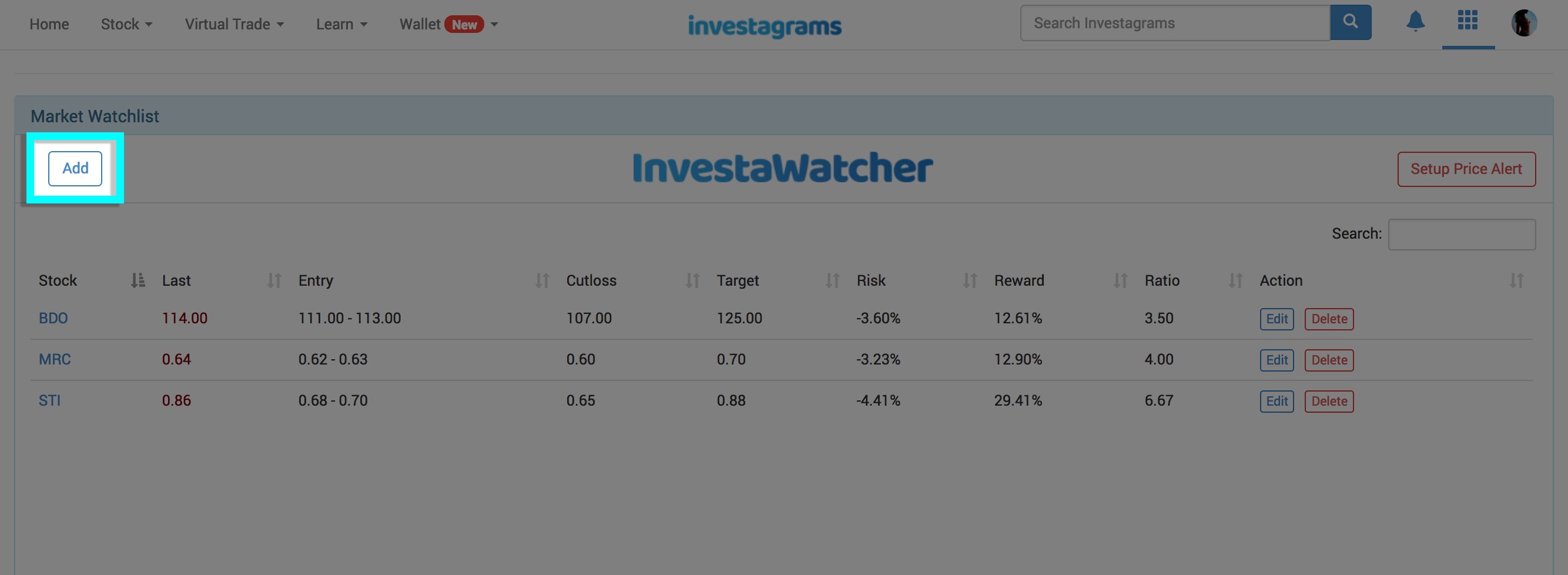

Once your payment has been confirmed, you can start adding stocks to your watchlist.

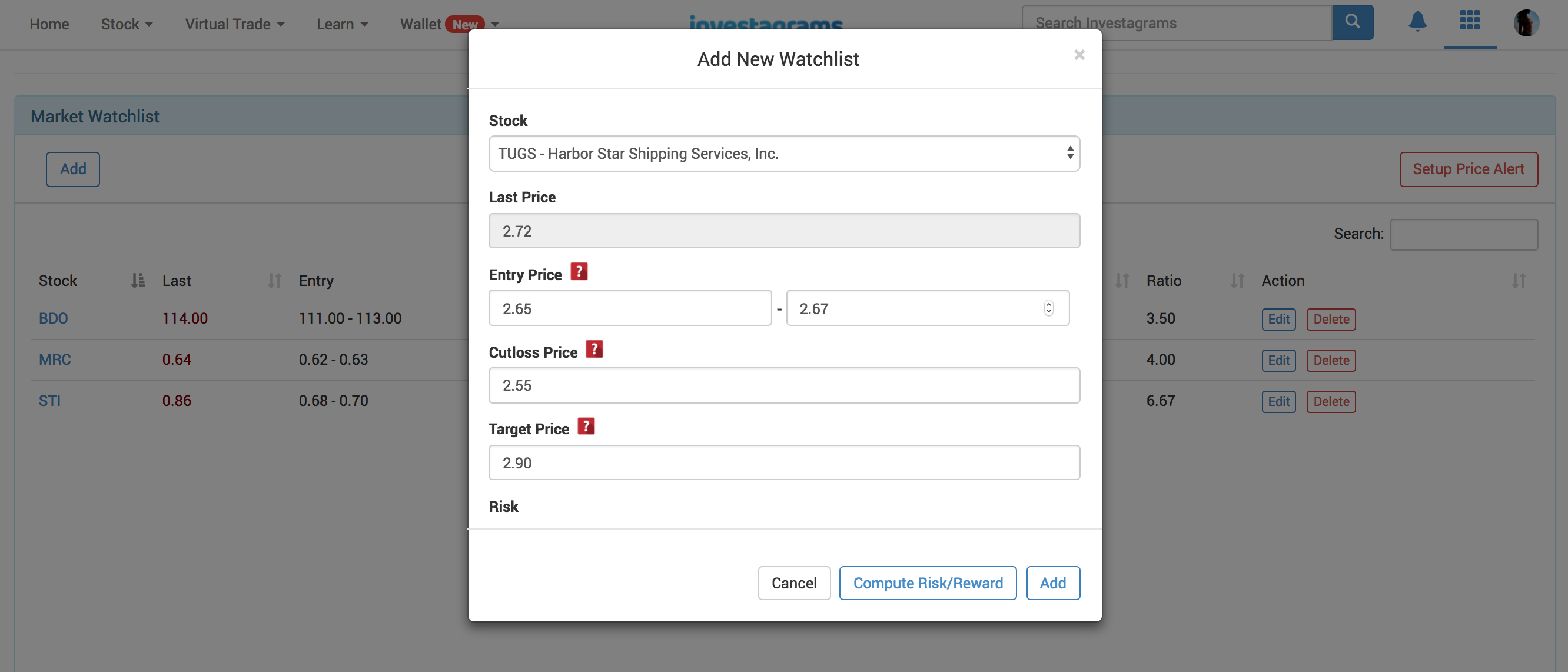

Simply go to your Investagrams account and click on the “Watcher” tool on the upper right corner.

Once you land on the InvestaWatcher page, click “Add” to start adding stocks to your watchlist.

A pop-up will appear for you to input your stock pick, entry, cutloss, and target prices:

Entry Price – The range of prices where you want to buy the stock. You will only receive an alert if the price hits this range. If the price jumps past your defined range, you will not receive an alert.

Cutloss Price – The price where you plan to cut your losses and sell your shares. You will receive an alert if the price reaches or falls below the number you enter.

Target Price – The price where you plan to sell your shares and realize your profit. You will receive an alert if the price reaches or goes higher than the number you enter.

Once you’ve entered all the information, click the “Add” button on the lower right of the box to finish setting up your stock.

Repeat this for all stocks you want to add to your watchlist. You can add up to 15 stocks.

STEP 3: CHOOSE HOW YOU GET YOUR ALERTS

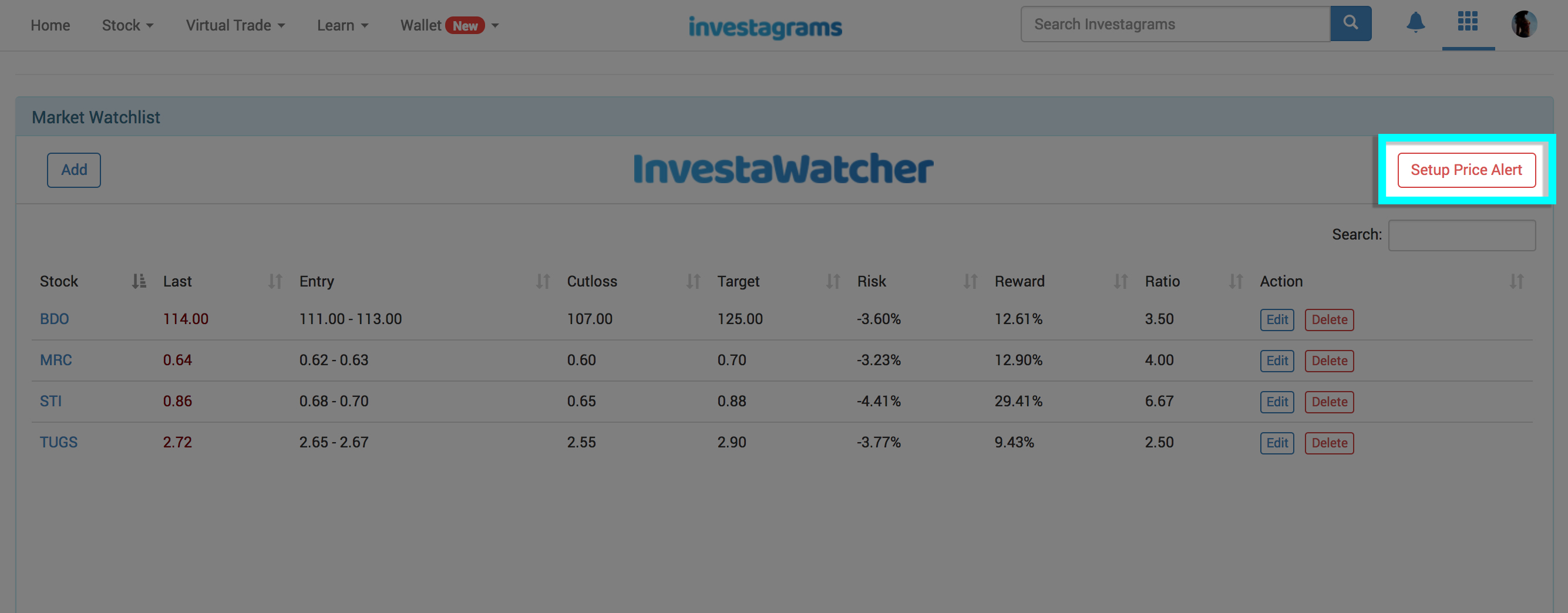

To customize how you get your alerts, just click on “Setup Price Alert” on the upper right corner of your InvestaWatcher page.

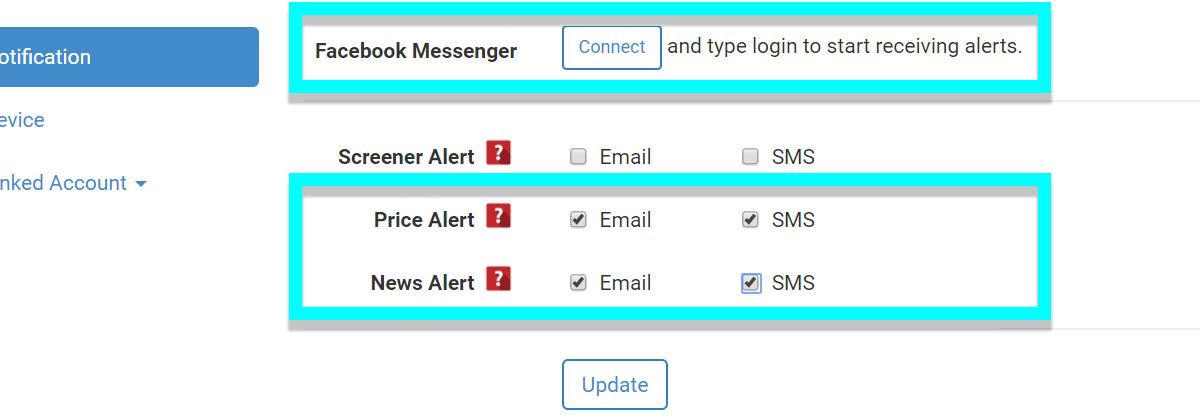

You will be taken to the settings page where you can choose which information you want to receive alerts on—price alerts only, news alerts only, or both. You can also turn alerts on or off for SMS, Facebook Messenger, and email.

That’s it! Now you can sit back and relax as we watch your stocks for you. Easy, right?

Not yet subscribed to InvestaWatcher? Click here to learn more and start hassle-free trading now!

You probably already know that the stock market is a great source of wealth. After all, it has created millionaires out of ordinary individuals, and it’s also where your banks, fund managers, insurance companies and even pension providers grow your money. However, you probably (or should) also know that it comes with risks, but is that alone a good reason to not invest? Are you actually safer financially if you didn’t invest your hard-earned money in places like the stock market?

“In a world that’s changing really quickly, the only strategy that is guaranteed to fail is not taking risks.” – Mark Zuckerberg, Founder & CEO of Facebook

Here’s the reality – kahit wala kang ginagawa, nababawasan yung totoong purchasing power ng pera mo kasi tumataas ang presyo ng lahat ng bilihin. With inflation spiking to as high as 6.4% and the interest we get for our savings at 0.25% – 0.50%, the glaring reality is that we are losing money just by leaving ALL of it in our savings.

Here are some of the simple yet powerful ways the stock market can generate wealth for you, and what you’re probably missing out on if you haven’t started investing!

CO-OWN AND GROW UP WITH THE COMPANIES

Companies don’t grow overnight. The Pinoy-favorite Jollibee ($JFC) started as an ice cream parlor in Quezon City in 1975, listed its shares for the first time at P9/share, and is now a global fastfood chain with stocks worth P270/share. Kung ginamit mo yung P10,000 mo to buy 1,000 shares at P10 each, that investment could have grown to ~P257,000 if you held onto the stock for over 2 decades. Imagine the huge potential if you set aside P10,000 every month to buy even more shares of the company!

But this story is old news. The truth is, none of us are time travelers; there’s no guarantee in knowing who will be the winners in 3, 5 or even 10 years from now. Otherwise, we’d all be rich! So it’s important to know the growth plans of the company. At present, we have the likes of Wilcon Depot ($WLCON) who is planning 24 new stores by 2020, from its 41 home depots in 2017. DoubleDragon Properties ($DD) plans to grow its leasable space by 3.7x to 1,200sq.m. in 2020. Ayala Land ($ALI) plans P40bn net earnings from real estate sales & rentals by 2020, from P25bn in 2017. These are only some among hundreds of listed companies with a vision to grow their business, so DON’T MISS OUT on the chance to ride alongside their growth!

COMPOUNDING DIVIDENDS

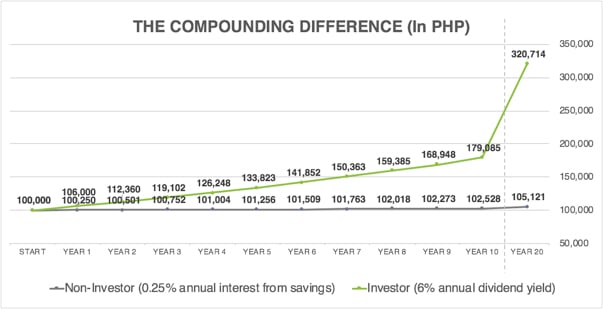

Another perk of growing up with companies is you get dividends, or a portion of their earnings. Re-invest the dividends you earn to buy more shares of the company (a.k.a Compounding), your P100k investment could grow to P320,714 in 20 years, assuming the company gives an annual dividend yield of 6%. That’s already worth a decent school tuition, if you plan to have kids!

Just this 2018, Globe ($GLO) has declared P91 in dividends per share, to be given in tranches. Semirara Mining Company ($SCC)’s dividend policy is 20% of prior year’s net income (attributable to common shareholders), while Pilipinas Shell ($SHLPH) intends to give out 70%. While dividend policies can still change depending on the company’s needs for expansion, growing up with companies that consistently declare dividends means that while you wait, you’re slowly getting returns for your investment.

BARGAIN-HUNTING

Bilhin mo nang mura, benta mo nang mahal. It’s what dealers and vendors do when they buy from cheap suppliers like Quiapo or Divisoria, and that’s essentially what Bargain-Hunting or Value Investing is about. Pero sa stock market, hindi mo kailangan umalis ng bahay para maghanap ng deals. You just need your laptop/smartphone, steady internet, and the willingness to learn the process.

An example of a cheap stock right now is First Gen ($FGEN), a provider of renewable energy and clean fuel. Its stock was beaten down heavily from its peak of P30/share back in 2015 to around P16/share as of writing. PLDT Inc. ($TEL) might also be a good example of a heavily beaten stock ever since news of a 3rd telco player threatened its market leadership, bringing its share price down from ~P3,100 in 2015 to < P1,500. While there’s no absolute guarantee that they will be able to recover, we do think renewable energy is an inevitable trend and despite our complaints with internet speed, you can’t get rid of PLDT so easily, so watch out for these and other bargains out there!

THE GAP

At this point you might wonder, ‘If the stock market presents a lot of profitable opportunities, why aren’t many Filipinos richer?’

Financial literacy still has a lot of catching up to do, given that there’s still a prevailing misconception that you are financially safe by avoiding any form of risk. Less than 1% of Filipinos are invested in the stock market, and we need your help in spreading its importance in empowering more Filipinos to take charge of their own finances. That is the mission of 2TradeAsia, who strives to make the investing experience easier and more digestible for everyone. Aside from a fast, seamless and reliable investing platform, they also offer actionable walkthroughs and step-by-step tutorials for those who are willing to learn the ropes on being their own fund manager.

With 2TradeAsia, you get all the tools you need to make informed decisions, and they even make themselves available on social media. If you haven’t started your stocks investing journey yet, chat them up on Facebook!

Share this article to your friends, and who knows – they might thank you in the future!

The biggest mistake we often see in most traders is focusing on which stock gives them more profits instead of learning how to find the best system that suits their trading lifestyle.

As with any business, one of the best moves every trader should do to be ahead in this industry is to take notes and analyze his/her trading experiences. One of the best moves every trader should do to be ahead in this industry is to take notes and analyze his/her trading experiences. The more documented evidence you have recorded into every single trade, the more you will learn about the market. The more you the better trader you can become.

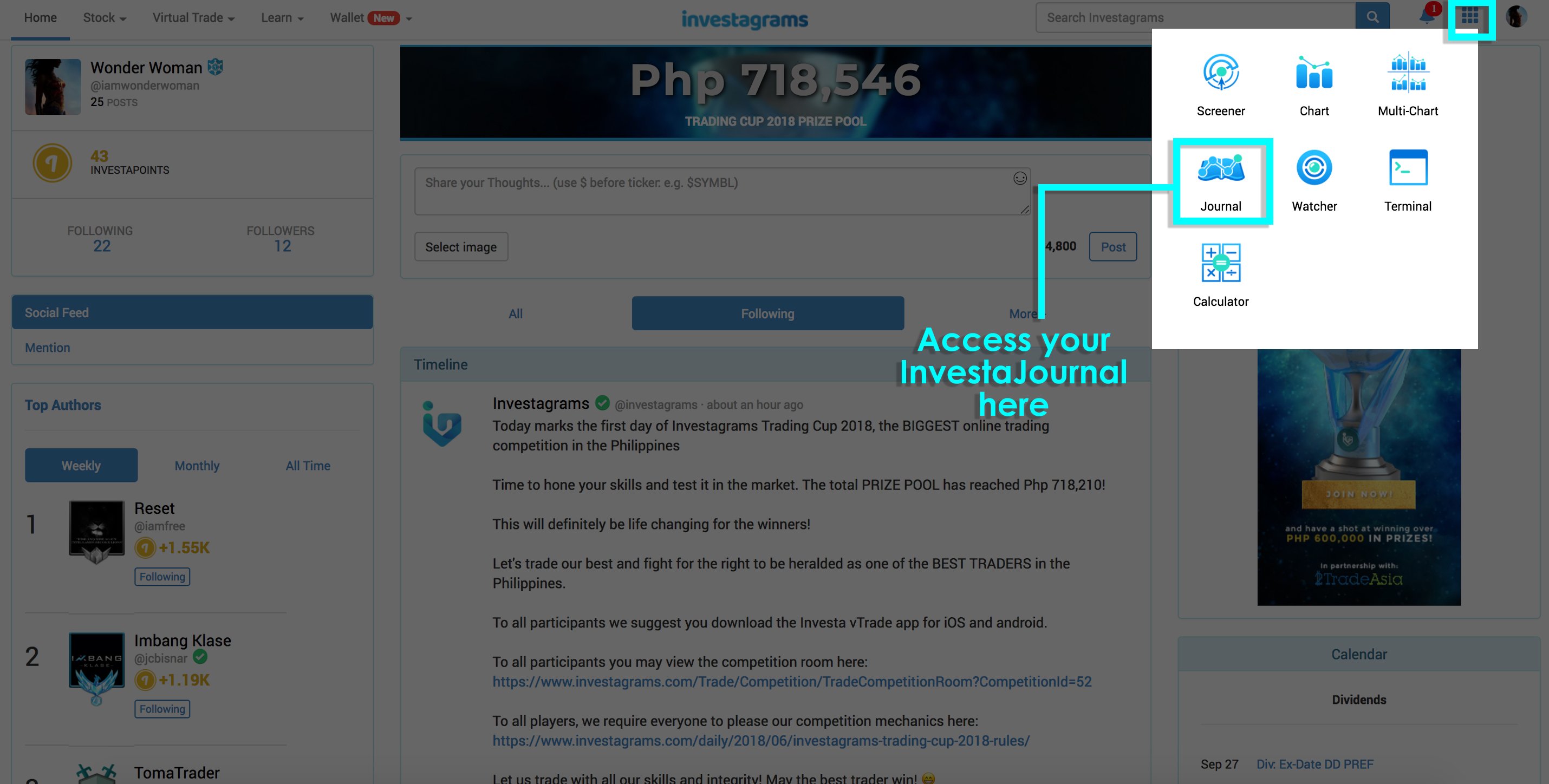

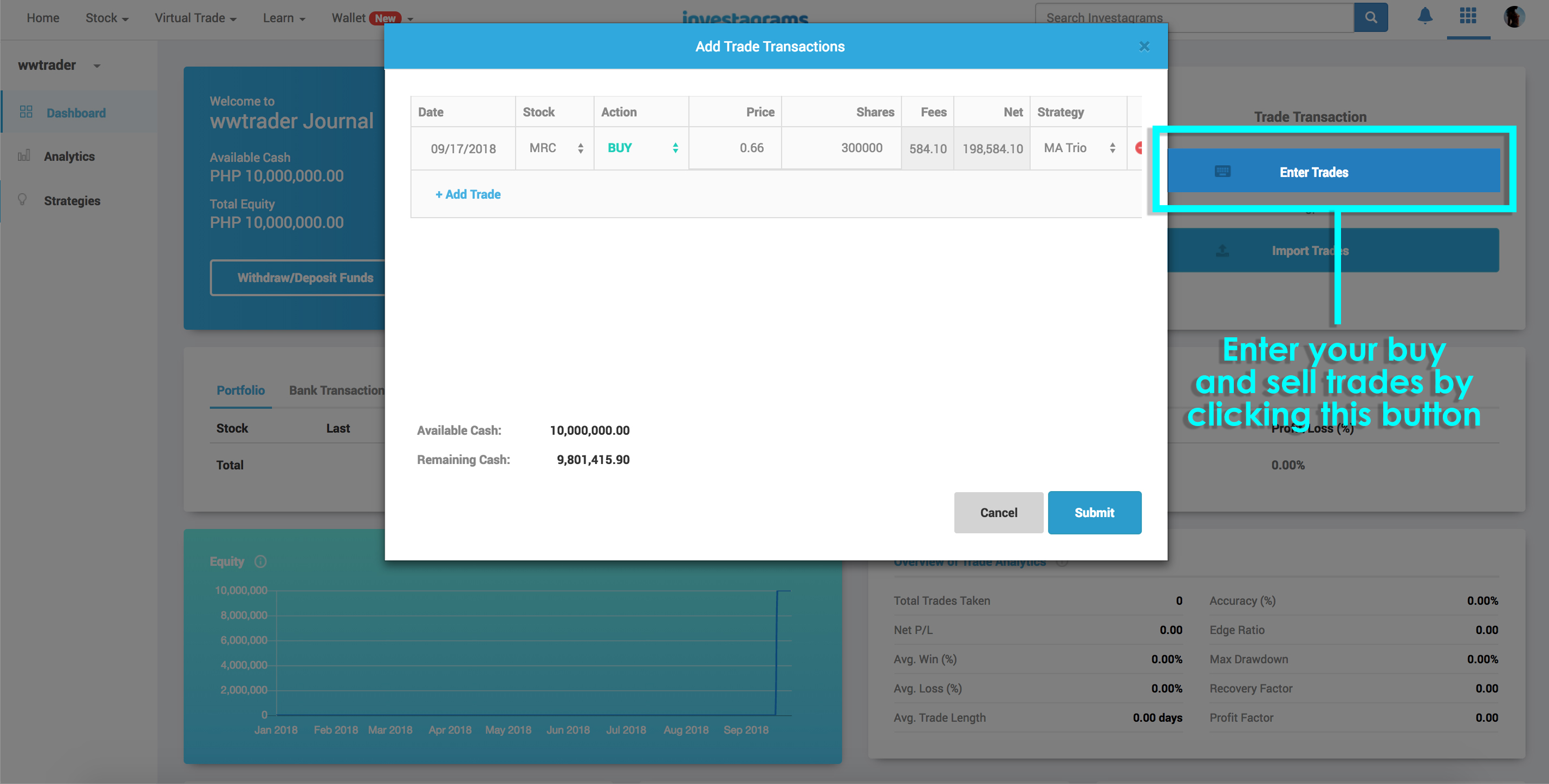

That’s why Investagrams brings you the newest and one of the most powerful tools every trader should have – the InvestaJournal where you can analyze and improve your personal strategies that will take you to the next level!

What is InvestaJournal?

InvestaJournal is a place to write your trading experience and record your way to success. It helps you to see your ability and your strategy through data and facts without any biases.

How it works

Anyone with Investagrams account can start and use the InvestaJournal as we are giving 10 days free trial to kick off this tool and get you started.

Features

Dashboard: It gives you an overview of all your trade transactions including analytics, strategy performance, top gainers and top losers

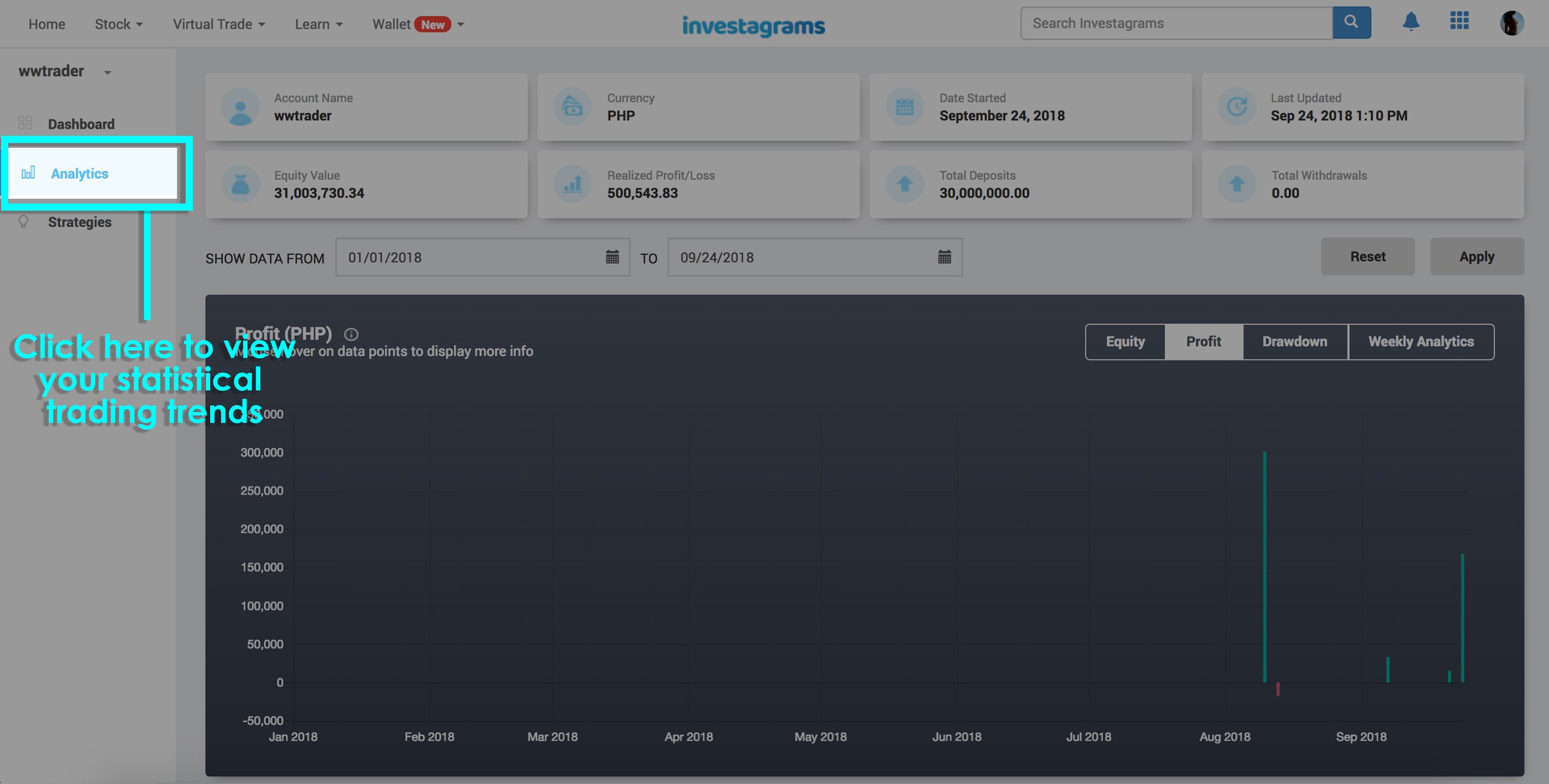

Analytics: Once you start getting your data trades, you can start learning about your performance as InvestaJournal automatically creates trends based on your inputs. A more detailed summary of trades that captures equity, profit, drawdown and weekly analytics is now accessible at your fingertips.

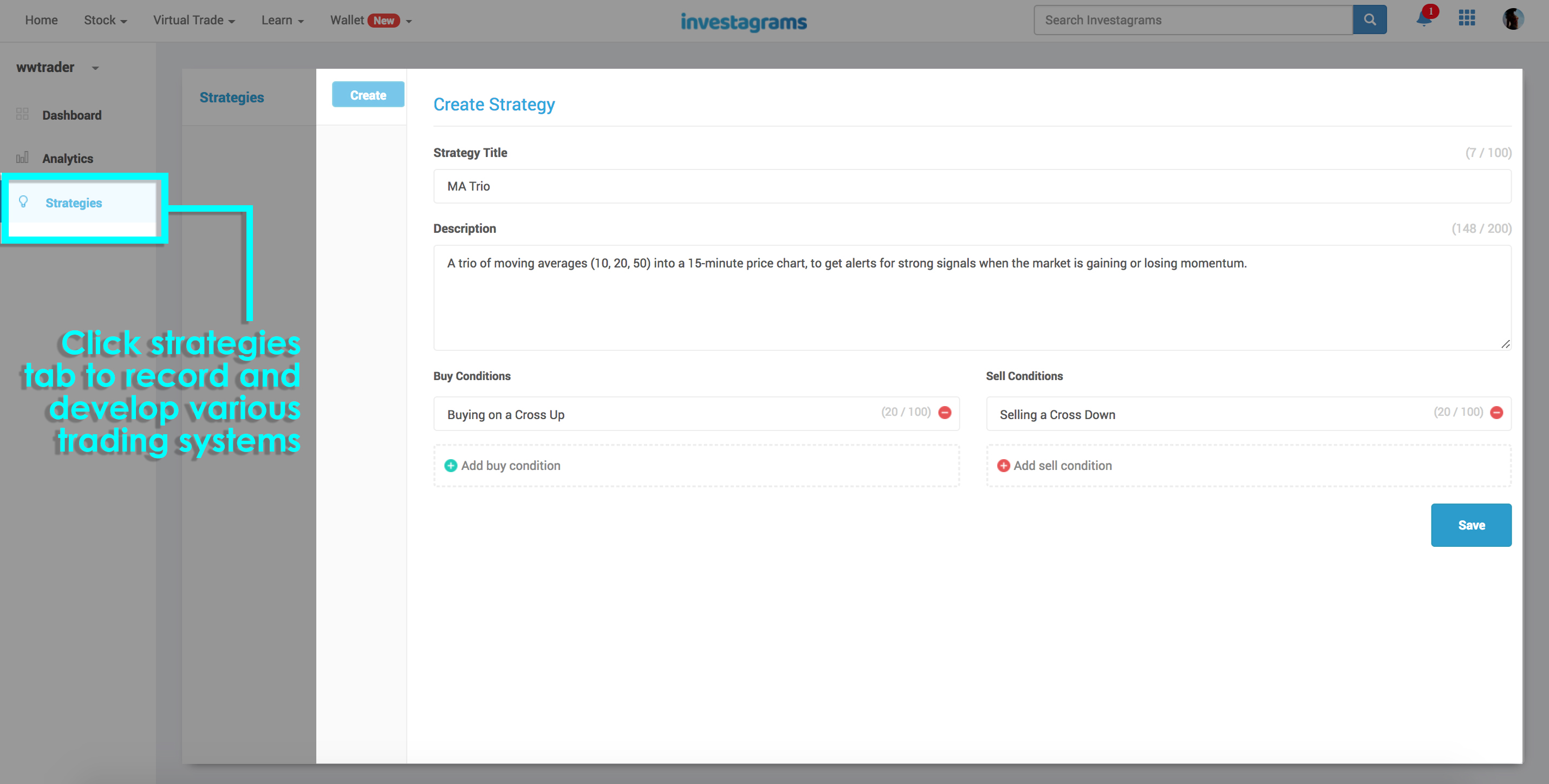

Strategies: You can log your trading strategies and thought processes behind each buy and sell you are making. This helps you remember what execution have you done and gives you a basis on fine-tuning your trading system.

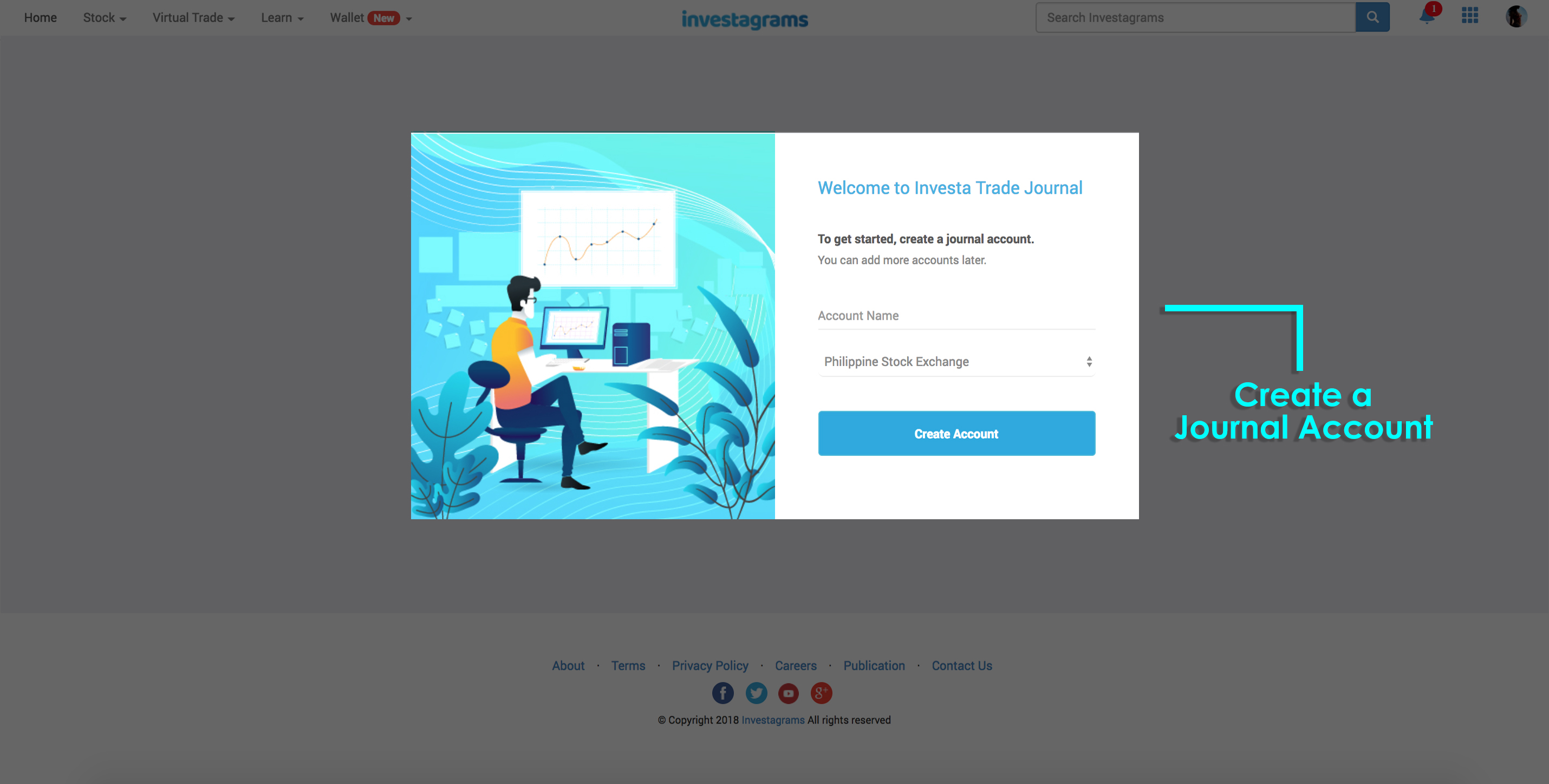

A new page will appear to create your Journal account with a username:

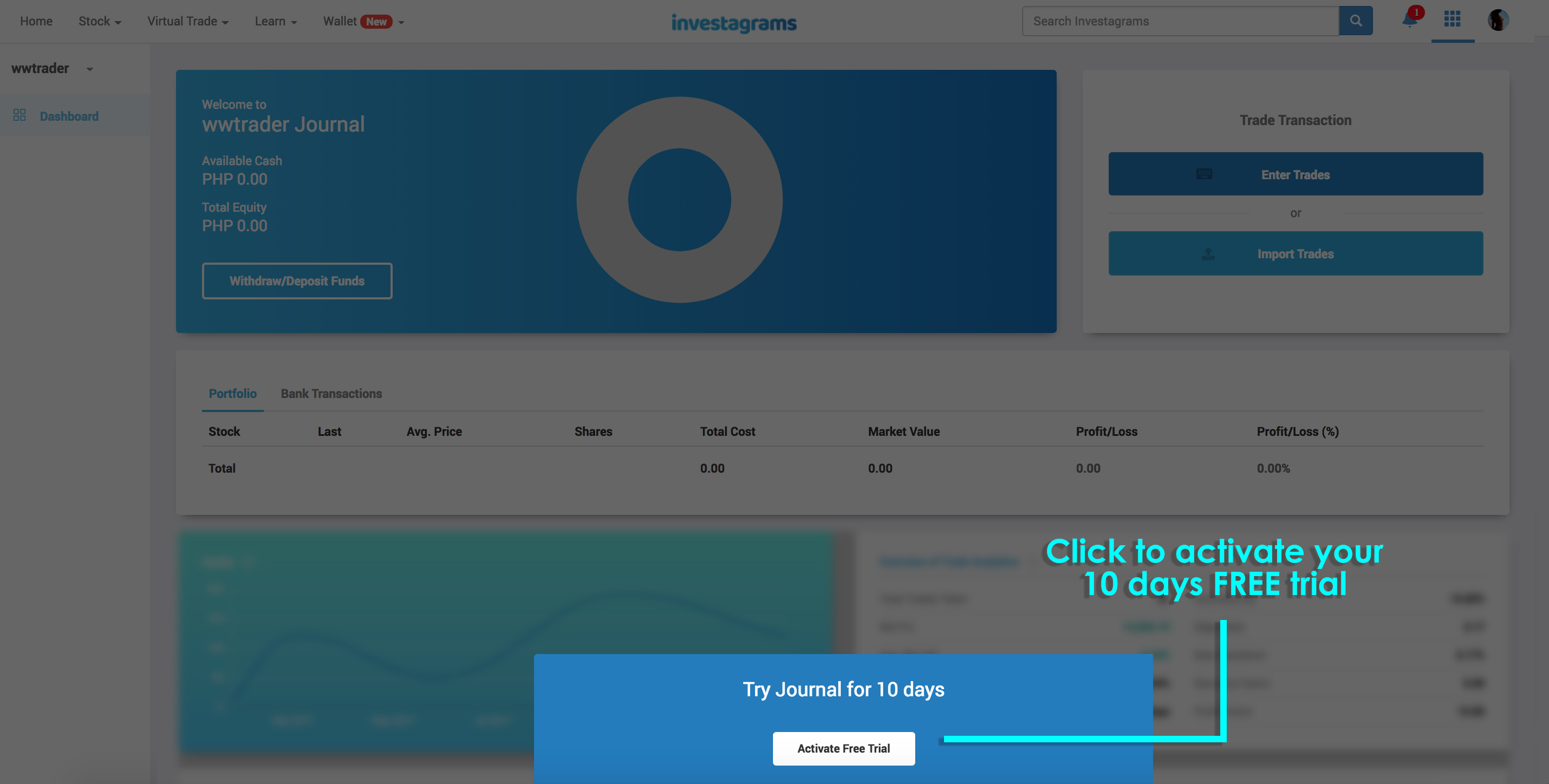

After account creation, a pop-up notice bar appears at the bottom page for activation of your 10 days FREE trial:

There are three necessary steps to try the InvestaJournal for free: There are three necessary steps to try the InvestaJournal for free:

Verify your email

Upload a valid ID

Start your free 10-day trial

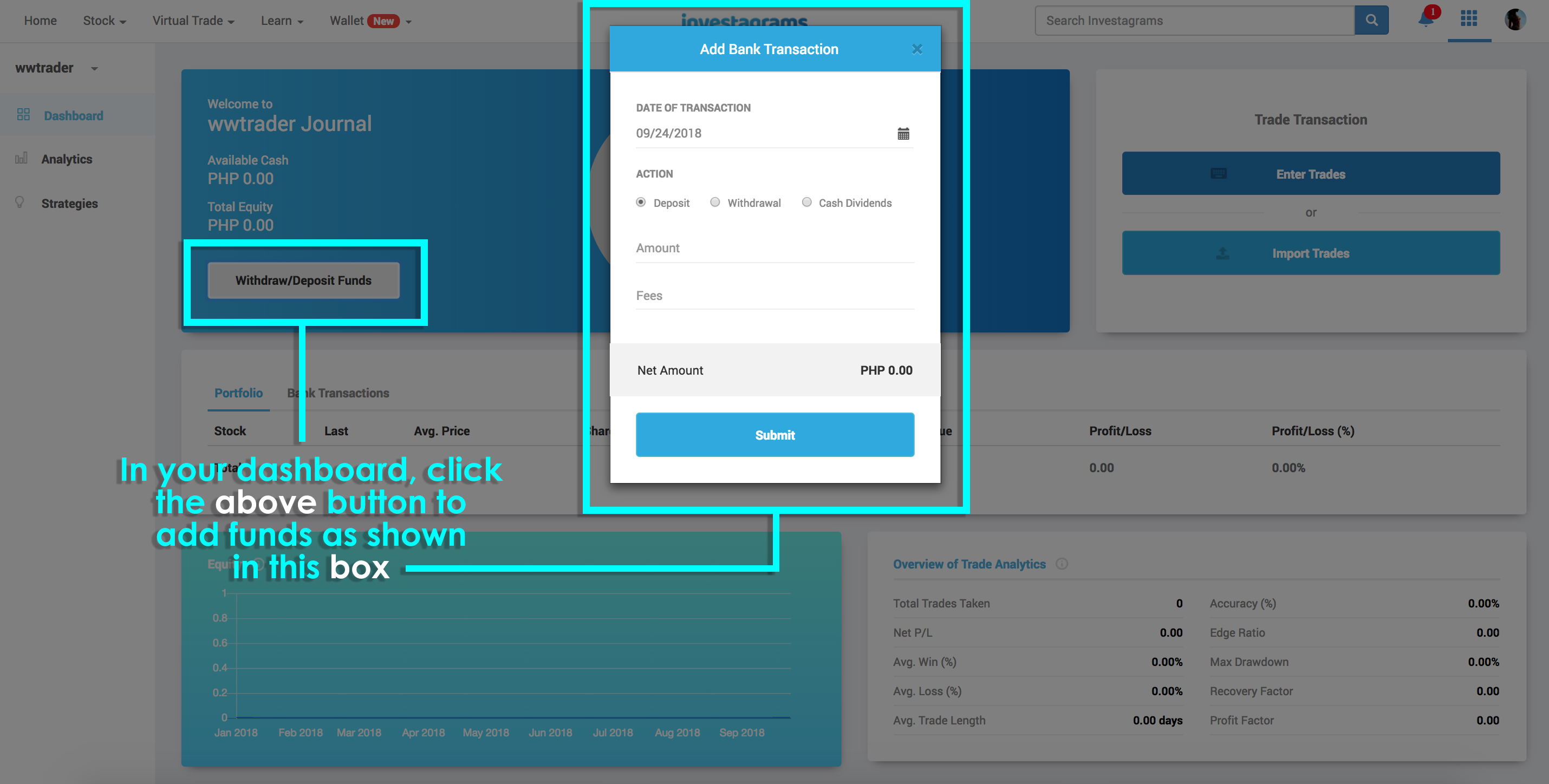

Once activated, you’ll be heading to the main dashboard and you can now start to log your funds (deposit, withdrawal or cash dividends) and your trades (buy, sell or stock div).

Identify your component and develop more discipline by recording all your strategies by logging your trading set-ups via the ‘Strategies’ tab:

Use the ‘Analytics’ tab to analyze how your decisions are impacting your trading performance:

Hope that helps! InvestaJournal features are built not only to find your edge, but to survive. It is a powerful combination of building your trade history and establish a trading routine that boost your lifestyle.

Support and resistance may be one of the most basic concepts in stock trading and technical analysis, but it is also one of the most useful. If you know how to use them well, you can already start building a profitable trading strategy. So here are 3 simple but powerful ways to use support and resistance in making profitable trades.

1. Find the best time to buy or sell your stocks.

This is a very basic use of support and resistance, but it is still one of the most effective.

The support and resistance levels often serve as an indicator of a coming shift or reversal of the current price movement. These levels serve as a guide for when we should start buying or selling a certain stock.

We buy stocks as the price nears the support level. Once it reaches the support, demand becomes stronger than supply and more people will want to buy that stock, making the price go up.

On the other hand, we sell stocks as the price gets closer to the resistance levels because this is when you can sell for the highest price. When the stock reaches the resistance level, more people will want to sell and the stock price will start going down again.

2. Identify stronger support and resistance by the length of time.

There are many support and resistance levels that can be found in a chart based on how long or short the time frame is. The longer the time frame, the stronger the support and resistance and the harder they are to break. In other words, a 10-year support or resistance is much stronger than a 1-month support or resistance.

Although the interpretation of a chart is subjective and different for everyone, seeing the bigger picture gives traders an idea of where the stock can go and how easy or difficult it will be for the stock to get there.

Next time you’re looking at support and resistance, try looking at the support and resistance across different time frames to see what the big picture really looks like.

3. Spot potential breakouts, which can lead to huge profits.

The resistance level, once broken, becomes the new support level. If sustained, it gives traders an idea that there is very strong demand for the stock. Breakouts like this usually signal the start of a major price trend, which can lead to huge profits.

This increased volatility during breakouts attract traders because it can offer great returns with a minimal amount of risk, especially if there is no existing resistance in place (i.e. when a stock breaks out to a new all time high).

Keep an eye out for breakouts and wait to see if they are sustained. If they are, it’s likely that you’ll be able to make a profit off of buying that stock.

Don’t forget, you can also combine these concepts to make your trading decisions.

For example, if you see that a stock has broken above its 10-year resistance, then you know from #2 and #3 above that it has the potential for huge profits and you should definitely consider buying that stock. If you want to buy a stock but it’s near its resistance level, then maybe wait a few days to get a better price.

Simple moves like this, applied consistently and with proper risk management will help you become a more profitable trader.

Do you have other tips and tricks for using support and resistance? Let us know in the comments below!

A lot of people ask us, “What is the best investment for beginners?” or “Saang investment ba yung ok?” There are so many options these days that it’s hard to figure out the difference between them all.

So how do you find the best investment for you? It all starts with getting to know yourself. Parang love lang yan. You can’t find your perfect match if you don’t know who you are and what you want. (What you really, really want.)

A lot of people would just say, “But I know what I want. I want to make as much money as possible!” Well, that’s the catch isn’t it? Do you know what’s possible given your current situation? Every person has different resources and abilities, so here are some questions you need to answer first before deciding where to invest:

1. How much money can you invest?

As the saying goes, you need money to make money. Each peso you invest is like a seed—the more seeds you have, the more trees you can grow, and the more fruits you can harvest. The more money you have to invest, the more money you can aim to make.

The amount of money you can invest will also determine which investment options are available to you. Investing is not only for the rich, but there are some investments that require a lot of capital.

A good rule of thumb to find out how much you can invest is to subtract 6 months worth of expenses from your savings. The remaining amount is what you can invest.

Total Savings – 6 Months of Expenses = Investment Fund

Every month, make sure you still have enough money to cover 6 months worth of living expenses before adding more money to your investment fund.

It’s important to keep your investment fund separate from your living expenses because investing is not a get-rich-quick scheme. It takes time. If you need to pull out your investment too soon, then you’ll likely end up losing money—and nobody wants that.

2. How long can you keep your money invested?

Aside from money, another very important resource when investing is time. The longer you’re willing to keep the money invested, the more investment options you’ll have and the more money you can potentially make.

Because of compounding interest, your money will grow exponentially faster every year you keep it invested. As the interest from your investment is added to the next year’s principal amount, the impact of compounding interest becomes so big that the amount of time eventually outweighs the amount money you invest.

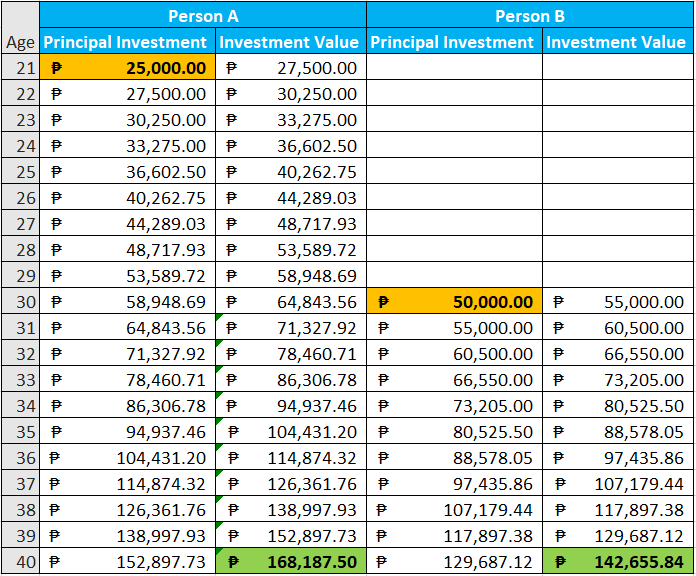

Here’s an example showing two investors, Person A and Person B. Person A invested P25,000 when he was 21 while Person B invested P50,000 when he was 30. Assuming the interest rate is always 10% for both cases, you’ll see that Person A’s investment will actually be worth more when they’re both 40 years old—even though Person B put in twice as much money.

When investing, think long-term. You’ll get the best results if you can invest your money for 10 years or more.

3. How much effort can you put into managing your investment?

If you have the time and dedication to educate yourself and manage your own investment, then you can save a lot on fees that would normally be paid to fund managers and financial advisers. It may even open up some investment opportunities that you couldn’t consider otherwise.

For example, a lot of people nowadays are marketing small businesses as investments—food carts and farming are just two examples. People will automatically ask “Ok ba ito?” and someone who has done it before might say “Oo! Laki ng return ko diyan!”

While it’s true that businesses can be great investments, they will only succeed if you put in the time and effort to run it well. Otherwise, you’ll just be throwing your money down the drain.

If you don’t have the time and energy to manage a high-maintenance investment, don’t worry. There are a lot of other investment options out there, which we’ll discuss later.

4. How much risk are you willing to take?

By now you’re probably tired of hearing this over and over, but it’s true—if you want bigger rewards, you’ll need to take on bigger risks. It’s difficult is to figure out exactly how much risk is right for you, but one thing’s for sure: There is no risk-free investment.

If you’re putting your money somewhere that’s risk-free, the interest rate will be so low that you end up losing money due to inflation. And if you’re losing money, then that’s not really an investment anymore.

Take savings accounts for example: Banks guarantee to keep your money safe and you definitely won’t lose a single centavo. However, the interest rate for most savings accounts is only 0.25%. That’s around 2.75% less than the average inflation rate, meaning that the value of your money decreases by 2.75% every year!

On the other hand, investing all your money in a new company that may or may not exist next year could lead you to lose all your money. But you might also have invested in the next Facebook and end up making a bigger profit than you ever dreamed of.

It’s always a balancing act when we talk about risk and reward, and the perfect mix is different for everyone. You need to take some time and really think about what would be the right balance for you.

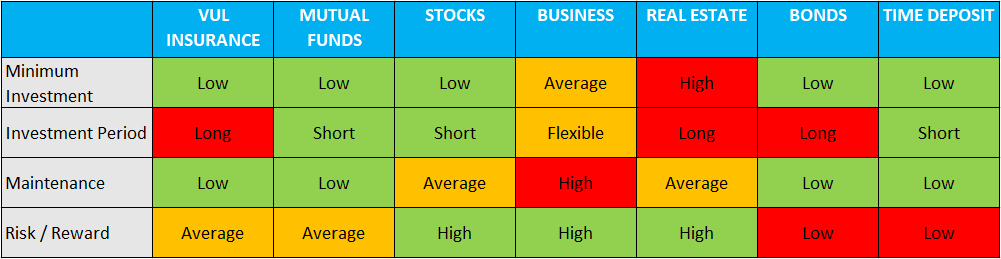

Main Investment Options in the Philippines

Here’s a table summarizing the main investments available in the Philippines, and what their characteristics are in relation to the four questions above.

If you find any of these interesting, then scroll down for more details.

VUL Insurance

VUL insurance plans are one of the most popular investment options in the Philippines. It’s a flexible and low-maintenance investment that hits three birds with one stone—life insurance, health insurance, and mutual funds. If you don’t have insurance yet, you should seriously consider getting VUL insurance.

Minimum Investment: VUL insurance plans are very flexible because they are personalized to your needs. You can have premiums that are as low as a couple thousand pesos per month. Just keep in mind that your benefits will be proportionate to the amount you invest.

Investment Period: Though there is some flexibility with VUL insurance, it’s best to aim for an investment period of at least 10 years. Most plans will deduct the largest fees in the first few years and let you invest for free by the 5th year or so.

Risk and Return: The risk profile and rate of return with VUL insurance is average overall, but can be adjusted based on your preference. Insurance companies usually have a few funds that cater to different risk profiles. Just make sure to get a good insurance agent so they can customize the best plan for you.

Recommended For: First-time investors who want an all-in-one package and don’t mind a long-term commitment

Mutual Funds

Mutual funds are another low-maintenance investment that is popular among Filipinos and especially working professionals. It has a lot of the same benefits as VUL insurance, but with two key differences: you won’t get any insurance (obviously) and you can think relatively more short-term. Put simply, mutual funds operate by pooling together money from many different investors and investing those in various assets and securities. That way it’s easier to diversify and manage risk.

Minimum Investment: Some mutual funds in the Philippines now have minimum investments as low as P5,000. The minimum investment will vary depending on which fund you’re looking at, but they’re all relatively low as far as investments go.

Investment Period: There is usually a lock-in period for mutual funds, though they can be as short as 90 days. You could even take out your investment earlier if you need to, but there will be a penalty. And of course as with any investment, you should think long-term if you want to see the biggest returns.

Risk and Return: Similar to VUL insurance, mutual funds have an average amount of risk and return. They can be higher or lower depending on the exact fund you choose, but professionally managed funds will be less risky than managing your own money.

Recommended For: Busy bees who just want to put their money somewhere where it can grow

Stocks

If you’re after bigger returns and don’t mind taking on a little more risk, then investing in stocks is a great way to go. It’s like the DIY counterpart to mutual funds. You’ll have to put more time and effort into managing your investment, but you’ll also have greater potential returns because you won’t have to pay any fund management fees.

Minimum Investment: Nowadays, you can open a stock trading account for as little as P2,500. Some brokerss won’t even require a minimum investment if you already have a savings account with their bank. Just keep in mind that, if you can afford it, we would still recommend start with at least P8,000. More on that here.

Investment Period: Stocks are very liquid investments, which means that it’s easy to sell, take your cash, and get out at any time. But keep in mind that even stocks require some time to earn substantial returns. There’s also a good chance that you will lose money if you need cash and have to sell your stocks at a loss. Always remember: Investments are not get-rich-quick schemes.

Risk and Return: Directly investing in stocks as an individual does carry more risk than VUL and mutual funds. Unlike professional fund managers, you won’t have a big corporation and fellow professionals helping you out. You’ll also have a smaller fund, which means you won’t be able to diversify your stock picks and manage risk as easily. Of course, the upside to all of this is that if you succeed, you’ll get to keep all the profits for yourself.

Recommended For: People who want bigger returns and are willing to dedicate time to managing their investment

Businesses

Minimum Investment: The initial investment for businesses varies a lot depending on the type of business you choose. It can be anywhere from a few thousand to a few million pesos. But whatever type of business you’re looking at, just remember that you’ll probably need enough cash to cover more than just the upfront cost. You’ll need to have enough money to cover costs for the first few months when your business may not be earning money yet. Not to mention, you’ll also need to invest a ton of time and effort if you want to give your business the chance to succeed.

Investment Period: It takes time for businesses to break even and earn a profit. While some only take a few months, others can take years. And either way, one thing’s for sure—there is no such thing as an overnight success. You’ll need to work hard and work consistently on building your business if you want any chance of seeing a return on your investment.

Risk and Return: A business is one of the riskiest investments you can make. It takes more work than any other investment, and even then a lot of businesses will fail within the first year of operations. But if you’re willing to take the risk, put in the work, and keep going despite the challenges, then your business could become a cash cow and the best investment you’ve ever made.

Recommended For: Strong-willed and self-motivated risk-takers who will do whatever it takes to succeed

Real Estate

There are two popular types of real estate investments in the Philippines—condos and land. There are some differences depending on which one you choose, but both don’t require that much maintenance and the potential return is quite high. If you can afford the high price tag, real estate might just be the right investment for you.

Minimum Investment: Depending on where the condo or piece of land is located, your cash out can be just a few hundred thousand pesos or a few million pesos. Compared to other options like stocks or mutual funds, you’ll definitely need to spend more money, but it could also pay off greatly.

Investment Period: With real estate, you can make money two ways: by renting out your property or through price appreciation. In both cases, it will take time for you to earn a profit. If you’re renting out a condo, you’ll likely have to hold on to your investment for at least 10 years before you recover your cost and start seeing returns. You could see returns faster if you’ve invested in land, but even this will depend heavily on the location of the land you’ve bought.

Risk and Return: Real estate is a high risk high reward type of investment. The initial cash out is very high compared to other investments, and it’s very difficult to sell if you suddenly need cash. Not to mention that even though the returns can be huge, they are not guaranteed. Investing in land is generally a bit safer than investing in a condo, but the demand for either can be unpredictable. Before investing in any property, make sure you do your research.

Recommended For: Seasoned investors looking to diversify their portfolio of assets and investments

Bonds

If you’re the conservative type of investor and don’t mind a lower rate of return, you can look into buying some bonds. When you buy bonds, you’ll know exactly how long you need to wait and you’ll also be guaranteed a certain rate of return. Just make sure that you can leave the money invested for the entire maturity period, because pulling out the investments early will mean losing money.

Minimum Investment: You can invest in retail treasury bonds (RTBs) for as low as P5,000, though many banks will require larger minimum investments. Because bonds have such low interest rates, then you may want to invest more if you can. That way, you’ll earn more actual pesos in profit.

Investment Period: Bonds will usually have longer investment periods that are a few years long, sometimes more. But the good thing is that you can find out the exact investment period upfront, even before you put out any money. Make sure you ask about the bond’s maturity date and that you won’t need the money before then.

Risk and Return: Both risk and return are very low for bonds, which is why they are recommended for conservative investors. Though your money won’t earn huge amounts of interest, at least you’re not likely to lose any money. At the very least, you’ll get an interest rate that’s higher than what you would get in a savings account.

Recommended For: Conservative and risk-averse investors whose main priority is not to lose money

Time Deposit

Time deposits are very similar to savings deposits, except that there is a specific date of maturity when you can take out your money. Because it’s such a low-risk investment, you can expect low returns as well. However, like bonds, this is another type of investment that will at least get you slightly more returns than a regular savings account.

Minimum Investment: The minimum investment for a time deposit can be as low as P1,000. But keep in mind that banks will usually give you a higher interest rate if you put in a larger investment.

Investment Period: The investment period for time deposits can also be very short—as short as 30 days. But again, keep in mind that banks will usually give you higher interest rates if you agree to a longer investment period.

Risk and Return: Time deposits usually have extremely low risk and extremely low returns. Some of them will have an interest rate that’s only 0.25% before tax—that’s the same as a regular savings account. But if you agree to a longer investment period or invest larger amounts of money then you can get a better interest rate. We recommend looking at other low-risk investment options too so you can decide if this is really the best option for you.

Recommended For: Extremely conservative investors who don’t have access to bonds or just prefer a more flexible low-risk investment

Conclusion

At the end of the day, anything that can make your money grow can be considered an investment. These definitely aren’t all the options, but we hope this helped you understand some of the most popular investments in the Philippines better. Only you can take this information and really look within yourself to find out what the best investment for you will be.

What are some of the best investments you’ve ever made? Let us know in the comments below!