Netflix is a company that has revolutionized the way people watch movies and television shows. It started as a mail-based DVD rental service in 1997, and evolved into a streaming platform that offers original content and a personalized recommendation system. How did Netflix achieve such success and growth? Here is a brief overview of its history and milestones.

Launch as a mail-based rental business (1997–2006)

Netflix was founded by Marc Randolph and Reed Hastings, two entrepreneurs who had previously worked at Pure Software, a software company. They came up with the idea of renting DVDs by mail after Hastings was charged a $40 late fee for returning a VHS tape of Apollo 13. They tested the concept by mailing a CD to Randolph’s house, and found that it arrived intact. They decided to launch Netflix as a website that offered a flat-fee unlimited rental model, with no due dates, late fees, or shipping charges. Customers could choose from a catalog of over 900 titles, and receive up to three DVDs at a time. Netflix also introduced a rating system that allowed customers to rate the movies they watched, and receive recommendations based on their preferences.

Netflix faced several challenges in its early years, such as competing with established video rental stores like Blockbuster, and dealing with the high costs of acquiring and distributing DVDs. However, Netflix managed to survive and grow by focusing on customer satisfaction, innovation, and efficiency. It also benefited from the increasing popularity and affordability of DVD players, which boosted the demand for its service. By 2002, Netflix had over one million subscribers, and went public on the NASDAQ stock exchange. By 2005, it had over four million subscribers, and a catalog of over 35,000 titles.

Transition to streaming services (2007–2012)

In 2007, Netflix launched its streaming service, which allowed subscribers to watch movies and TV shows instantly on their computers, or on devices such as game consoles, smart TVs, and Blu-ray players. This was a major shift for the company, as it moved from a physical to a digital distribution model. Netflix also expanded its content library by licensing movies and shows from studios and networks, such as Disney, Paramount, Sony, NBC, and CBS. Netflix also partnered with Starz, a premium cable channel, to offer its subscribers access to more than 1,000 movies and shows, including new releases and exclusives.

Netflix’s streaming service quickly gained popularity, as it offered convenience, variety, and value to its customers. By 2010, Netflix had over 20 million subscribers, and accounted for more than 20% of the Internet traffic in North America. However, Netflix also faced some challenges and controversies, such as increasing competition from other streaming services, such as Hulu and Amazon Prime Video, and rising costs of licensing content from studios and networks, who saw Netflix as a threat to their traditional business models. In 2011, Netflix announced a controversial decision to split its DVD and streaming services into two separate plans, and raise its prices by up to 60%. This caused a backlash from many customers, who felt betrayed and angry. Netflix lost over 800,000 subscribers, and its stock price plummeted by more than 75%. Netflix apologized for its poor communication, and reversed its decision to split its services, but kept its price increase.

Development of original programming (2013–2017)

In 2013, Netflix made a bold move by producing and releasing its own original content, starting with House of Cards, a political drama series starring Kevin Spacey and Robin Wright. The show was a critical and commercial success, and won several awards, including Emmys and Golden Globes. Netflix followed up with more original shows, such as Orange Is the New Black, a comedy-drama series set in a women’s prison, and Stranger Things, a sci-fi horror series set in the 1980s. Netflix also ventured into other genres, such as documentaries, stand-up comedy, animation, and foreign language shows. Netflix also acquired the rights to some existing shows, such as Arrested Development, Black Mirror, and The Crown, and continued their production as Netflix originals.

Netflix’s original content strategy proved to be a game-changer, as it gave the company more control over its content, and more differentiation from its competitors. It also attracted more subscribers, who were drawn to the quality, diversity, and exclusivity of Netflix’s shows. By 2017, Netflix had over 100 million subscribers worldwide, and spent over $6 billion on original content. Netflix also received more recognition and acclaim, as it earned more nominations and awards than any other network or streaming service.

Expansion and diversification (2018–present)

In 2018, Netflix continued to expand and diversify its content and operations, as it faced more competition and challenges in the streaming market. Netflix increased its investment in original content, and produced more than 700 shows and movies, including Roma, a Spanish-language film directed by Alfonso Cuarón, which won three Oscars, and Bird Box, a thriller starring Sandra Bullock, which was watched by over 80 million households in its first month. Netflix also expanded its international presence, and launched more local and regional content, such as Sacred Games, an Indian crime thriller series, and The Witcher, a fantasy series based on a Polish book series. Netflix also experimented with new formats and features, such as interactive shows, such as Black Mirror: Bandersnatch, which allowed viewers to choose their own storylines, and mobile-only plans, which offered cheaper subscriptions for users who only watched on their smartphones.

Netflix also faced some challenges and controversies, such as losing some of its licensed content, such as Friends and The Office, to other streaming services, such as HBO Max and Peacock, and facing more competition from new entrants, such as Disney+, Apple TV+, and Paramount+. Netflix also faced some legal and regulatory issues, such as being sued by the estate of Arthur Conan Doyle for its portrayal of Sherlock Holmes in Enola Holmes, and being banned in some countries, such as China and Saudi Arabia, for its content or policies. Netflix also faced some criticism and backlash, such as being accused of promoting pedophilia for its film Cuties, and being boycotted by some users for its support of the Black Lives Matter movement.

Despite these challenges and controversies, Netflix remained the dominant and most popular streaming service in the world, with over 200 million subscribers, and over $25 billion in revenue. Netflix also continued to innovate and improve its service, by introducing new features, such as Shuffle Play, which randomly selected a show or movie for users to watch, and Top 10, which ranked the most popular titles in each country. Netflix also continued to produce and release more original and diverse content, such as The Queen’s Gambit, a chess drama series starring Anya Taylor-Joy, and The Social Dilemma, a documentary that explored the impact of social media on society.

Netflix is a company that has changed the way people watch and enjoy movies and TV shows. It has also changed the way content is created and distributed, by offering more creative freedom and opportunities to filmmakers and actors. Netflix has also influenced the culture and society, by creating and promoting content that reflects and challenges the issues and values of the times. Netflix is a company that has a story worth telling, and worth watching.

Retiring early is a dream for many people who want to enjoy more freedom, leisure, and fulfillment in life. However, retiring early also requires careful planning, saving, and investing, as well as a willingness to make some trade-offs and sacrifices. In this article, we will explore how it is possible to retire early, what are the benefits and challenges of early retirement, and what are some tips and strategies to achieve it.

What does it mean to retire early?

Retiring early means leaving the workforce before the conventional retirement age of 60 or 65. There is no fixed definition of what constitutes early retirement, as it depends on various factors such as your income, expenses, lifestyle, goals, and health. However, a common way to measure early retirement is by using the concept of financial independence, which means having enough savings and investments to cover your living expenses for the rest of your life, without relying on a job or pension.

How to achieve early retirement?

Achieving early retirement is not easy, but it is not impossible either. It requires a combination of earning, saving, and investing, as well as a clear vision of what you want to do in retirement. Here are some steps to follow to retire early:

Define your retirement goals:

Before you start saving and investing, you need to have a clear idea of what you want to do in retirement, how much it will cost, and when you want to retire. You can use online calculators or tools to estimate your retirement needs and timeline, based on your current income, expenses, savings, and expected returns.

Increase your income:

The more you earn, the more you can save and invest for retirement. You can increase your income by advancing your career, developing new skills, starting a side hustle, or creating passive income streams. You can also look for ways to reduce your taxes, such as contributing to tax-advantaged accounts or claiming deductions and credits.

Reduce your expenses:

The less you spend, the more you can save and invest for retirement. You can reduce your expenses by living below your means, budgeting, tracking your spending, and cutting unnecessary costs. You can also look for ways to save on housing, transportation, food, utilities, insurance, and entertainment.

Invest wisely:

The more you invest, the faster you can grow your wealth and reach your retirement goals. You can invest wisely by diversifying your portfolio, choosing low-cost and tax-efficient funds, taking advantage of compound interest, and rebalancing your asset allocation. You can also follow the 4% rule, which states that you can withdraw 4% of your portfolio value each year in retirement, without running out of money.

Adjust your lifestyle:

The more flexible you are, the easier it will be to retire early. You can adjust your lifestyle by being open to new opportunities, experiences, and challenges, as well as being willing to make some trade-offs and sacrifices. You can also consider relocating to a cheaper or more tax-friendly location, downsizing your home, traveling on a budget, or pursuing your passions and hobbies.

What are the benefits and challenges of early retirement?

Early retirement has both benefits and challenges, and you need to weigh them carefully before making your decision. Here are some of the pros and cons of early retirement:

– Benefits: Early retirement can offer you more freedom, leisure, and fulfillment in life. You can have more time and energy to pursue your interests, hobbies, passions, and goals, as well as to spend with your family and friends. You can also have more control over your schedule, pace, and location, and enjoy a healthier and happier lifestyle.

– Challenges: Early retirement can also pose some financial, emotional, and social risks. You may face a higher risk of running out of money, especially if you encounter unexpected expenses, inflation, market downturns, or health issues. You may also face a loss of identity, purpose, and structure, as well as a reduced social network and support system, after leaving your job. You may also have to deal with boredom, loneliness, isolation, or depression, if you do not have meaningful activities or relationships to fill your time.

Conclusion

Retiring early is possible, but it requires careful planning, saving, and investing, as well as a clear vision of what you want to do in retirement. By following the steps outlined in this article, you can achieve early retirement and enjoy more freedom, leisure, and fulfillment in life. However, you also need to be aware of the benefits and challenges of early retirement, and be prepared to face them with confidence and resilience.

Central banks are powerful institutions that play a vital role in shaping economic conditions. They have the responsibility of managing the money supply, setting interest rates, ensuring financial stability, and implementing monetary policy. In this article, we will explore how central banks influence the economy and why their actions matter for businesses and consumers.

What is a central bank?

A central bank is a financial institution given control over the production and distribution of money and credit. Its primary function is to manage the nation’s money supply (monetary policy), controlling inflation, printing money, setting interest rates, maintaining the health of the financial system, and ensuring economic stability.

Central banks are usually independent from the government, meaning that they are not subject to political interference or pressure. This allows them to pursue their objectives without being influenced by short-term political agendas or interests. However, central banks are still accountable to the public and the government. They have to explain and justify their decisions and actions.

How do central banks control the money supply?

Central banks control the amount of money circulating in the economy by using various tools, such as open market operations, reserve requirements, and interest rate adjustments.

Open market operations

This is the process of buying or selling government securities (such as bonds or treasury bills) in the open market. When the central bank buys securities, it pays with new money, increasing the money supply. When it sells securities, it takes money out of circulation, decreasing the money supply.

Reserve requirements

This is the percentage of deposits that commercial banks have to keep as reserves. The higher the reserve requirement, the less money banks can lend out, reducing the money supply. The lower the reserve requirement, the more money banks can lend out, increasing the money supply.

Interest rate adjustments

This is the rate at which the central bank lends money to commercial banks. The higher the interest rate, the more expensive it is for banks to borrow money. This discourages lending and reduces the money supply. The lower the interest rate, the cheaper it is for banks to borrow money. Thus, encouraging lending and increasing the money supply.

How do central banks influence the economy?

Central banks influence the economy by affecting the cost and availability of money and credit. In turn affecting the spending and investment decisions of businesses and consumers. By controlling the money supply and interest rates, central banks can influence the rate of inflation, the level of economic activity, and the exchange rate of the currency.

Inflation

This is the general increase in the prices of goods and services over time. Central banks aim to keep inflation low and stable. High and volatile inflation can erode the purchasing power of money, distort economic signals, and create uncertainty and instability. Central banks use monetary policy to manage inflation, by adjusting the money supply and interest rates. When inflation is above the target, the central bank tightens monetary policy. This is done by reducing the money supply and raising interest rates. When inflation is below the target, the central bank eases monetary policy. This makes borrowing and spending cheaper, stimulating the economy and raising inflation.

Economic activity

This is the level of production, consumption, and trade in the economy, measured by indicators such as gross domestic product (GDP), unemployment, and industrial output. Central banks aim to support economic growth and employment. They also use monetary policy to influence economic activity, by affecting the demand and supply of money and credit. When economic growth is strong, the central bank tightens monetary policy, by reducing the money supply and raising interest rates. This cools down the economy, preventing overheating and high inflation. When economic growth is weak, the central bank eases monetary policy, by increasing the money supply and lowering interest rates. This boosts the economy, preventing deflation and recession.

Exchange rate

This is the price of one currency in terms of another currency, determined by the supply and demand of currencies in the foreign exchange market. Central banks can affect the exchange rate of their currency, by changing the money supply and interest rates. When the central bank increases the money supply and lowers interest rates, the domestic currency becomes less attractive. This causes the currency to depreciate, meaning that it becomes cheaper relative to other currencies. The opposite also holds true. Higher rates often causes the domestic currency to appreciate.

Why do central banks matter for businesses and consumers?

Central banks matter for businesses and consumers, as their actions have direct and indirect effects on the economy and the financial system. By influencing the money supply, interest rates, inflation, economic activity, and exchange rates, central banks affect the cost and availability of credit, the profitability and competitiveness of businesses, the income and spending power of consumers, and the stability and confidence of the economy.

Cost and availability of credit

This is the price and quantity of loans and other forms of borrowing in the economy. Central banks affect the cost and availability of credit, by changing the interest rate and the money supply. When the central bank lowers the interest rate and increases the money supply, credit becomes cheaper and more abundant, making it easier for businesses and consumers to borrow and spend. This can stimulate economic growth and investment, but also increase the risk of excessive debt and inflation. When the central bank raises the interest rate and decreases the money supply, credit becomes more expensive and scarce, making it harder for businesses and consumers to borrow and spend. This can slow down economic growth and investment, but also reduce the risk of overheating and inflation.

Profitability and competitiveness of businesses

This is the ability of businesses to generate revenues and profits. Central banks affect the profitability and competitiveness of businesses, by affecting the inflation, economic activity, and exchange rate of the currency. When the central bank keeps inflation low and stable, businesses can plan and invest with more certainty and confidence, as they face lower costs and risks. They can also impact businesses by causing catalysts in the forex market. A stronger currency can make exports more expensive and imports cheaper, hurting exporters and benefiting importers. A weaker currency can make exports cheaper and imports more expensive, helping exporters and hurting importers.

Income and spending power of consumers

This is the amount and value of money that consumers earn and spend in the economy. Central banks affect the income and spending power of consumers, by affecting the interest rates, inflation, economic activity, and exchange rate of the currency. When the central bank lowers interest rates and increases the money supply, consumers can benefit from lower borrowing costs and higher asset prices, as they can access cheaper credit and increase their wealth. The central bank keeps inflation low and stable, consumers can preserve the purchasing power of their money, as they face lower prices and costs. As they support economic growth and employment, consumers can enjoy higher income and job security, as they have more opportunities and confidence to work and earn. When the central bank influences the exchange rate of the currency, consumers can gain or lose purchasing power, depending on whether the currency appreciates or depreciates. A stronger currency can make foreign goods and services cheaper, increasing the purchasing power of consumers. A weaker currency can make foreign goods and services more expensive, decreasing the purchasing power of consumers.

Stability and confidence of the economy

This is the degree of certainty and trust that the economy and the financial system are functioning well and can withstand shocks and crises. Central banks affect the stability and confidence of the economy, by ensuring the financial stability of the banking system, implementing credible and transparent monetary policy, and coordinating with other central banks and authorities. When the central bank ensures the financial stability of the banking system, it prevents bank failures and systemic risks, by monitoring and regulating the financial institutions, providing liquidity and emergency loans, and acting as a lender of last resort. As they implement credible and transparent monetary policy, they enhance the effectiveness and predictability of their actions.

Conclusion

Central banks are influential institutions that have a significant impact on the economy and the financial system. They control the money supply, set interest rates, ensure financial stability, and implement monetary policy. By doing so, they influence the inflation, economic activity, and exchange rate of the currency. Their actions affect the cost and availability of credit, the profitability and competitiveness of businesses, the income and spending power of consumers, and the stability and confidence of the economy. Central banks matter for businesses and consumers, as they shape the economic conditions and environment in which they operate and live.

A zero-sum game is a situation where one party’s gain or loss is exactly balanced by the losses or gains of another party or parties. It is a concept that is often used in game theory, economics, and business to analyze the outcomes and strategies of different players in a competitive scenario. In a zero-sum game, the total benefit or cost of all the players is always zero, meaning that there is no net change in wealth or value. For every winner, there is a loser of equal magnitude.

Examples of Zero-Sum Games

Zero-sum games can be found in many contexts, both in real life and in theoretical models. Some examples of zero-sum games are:

Poker and gambling

In these games, the amount of money won by some players is equal to the amount of money lost by the others. The net change in the total money of all the players is zero.

Futures and options trading

In these financial instruments, the contracts represent agreements between two parties that are based on the price of an underlying asset. For every investor who makes a profit on a contract, there is another investor who suffers a loss of equal value. The net change in the total wealth of all the investors is zero.

Zero-Sum vs. Non Zero-Sum Games

Zero-sum games are the opposite of non zero-sum games, where the total benefit or cost of all the players is not zero, meaning that there is a net change in wealth or value. In non zero-sum games, the outcome can be beneficial or detrimental to all the players, or to some of them. Non zero-sum games are more common and realistic than zero-sum games, as they reflect the complexity and interdependence of real-world situations. Some examples of non zero-sum games are:

Trade and exchange

In these situations, two or more parties agree to exchange goods or services that they value differently. By doing so, they can both increase their utility or satisfaction, creating a positive sum game. For example, if Alice trades her apples for Bob’s bananas, and they both prefer the fruit they receive, they both gain from the trade.

Public goods and externalities: In these situations, the actions of one or more parties affect the welfare of others, without being reflected in the market price or cost. This can create positive or negative externalities, which are benefits or costs that are not internalized by the parties involved. For example, if a factory pollutes the air, it imposes a negative externality on the society, as it reduces the quality of life and health of the people. On the other hand, if a farmer plants trees, it creates a positive externality, as it improves the environment and the climate.

Implications of Zero-Sum Games

Zero-sum games have important implications for the behavior and decision-making of the players involved. They are competitive and adversarial, as the players have conflicting interests and goals. The players have to act strategically and rationally, taking into account the actions and reactions of the other players. The players may also try to deceive or manipulate the other players to gain an advantage.

Zero-sum games are often solved with the minimax theorem or the Nash equilibrium, which are concepts that determine the optimal strategy for each player, given the strategies of the other players. The minimax theorem states that a player should choose the strategy that minimizes the maximum possible loss, while the Nash equilibrium states that a player should choose the strategy that maximizes the expected payoff, assuming that the other players do the same.

Zero-sum games are not conducive to cooperation or collaboration, as the players have no incentive to work together or share information. The players may also face a dilemma or a paradox, where the individually rational choice leads to a collectively irrational outcome. For example, in the prisoner’s dilemma, the dominant strategy for each prisoner is to defect, but this results in a worse outcome for both prisoners than if they both cooperated.

Is Trading a Zero-Sum Game?

Yes, and no. In an environment where market participants are all fighting for fluctuations or price movements, this does create a zero-sum game scenario. In markets like the forex market or futures, most traders often just earn through capital gains which doesn’t lead to the creation of wealth.

However, things change when shares of companies are the assets being traded. While there will be traders who are looking to profit from price swings, there are also long term investors who aren’t looking to gain through quick trades. By pursuing gains through dividends or the overall growth of the company, the dynamics change from traders simply fighting for money between each other to the exchange of goods and services between market participants.

The overall lesson here being that fundamentals play a vital role in the stock market as it dictates whether a stock has the capacity to generate wealth. Something that will determine if the trading of shares will remain a zero-sum game.

This competition is OPEN TO ALL and will run for three months from April 22, 2024 to August 26, 2024

1. Registration. The competition officially begins on April 22, 2024 (Monday). You will receive a notification once you have been automatically added to the Competition Room and the Trading Cup is about to begin. Click here to join the competition.

Important notes:

Verification of ID is required before the competition starts. Once you are verified, you will be able to access the learning modules via InvestaUniversity, and in addition, this ID will be used to verify the winner’s identity during the awarding of prizes. Winners who did not send us a valid ID will be disqualified.

Only one (1) entry and account per person is allowed. If you have more than 1 account to join the competition, you will be immediately DISQUALIFIED.

You can change your Display Name, Username, and Profile Picture until THE DAY BEFORE the competition starts. Once the Trading Cup begins, the system will not allow you to change the above mentioned anymore.

2. Platform. The participants of Trading Cup 2024: The Global Quest will use the Virtual Trading Platform or vTrade of Investagrams which tracks the real-time price movements in the Philippine Stock Exchange (PSE), US Market, and Crypto Market.

3.New Markets. For the first time in Trading Cup history, we will now add the GLOBAL MARKETS, specifically the US Market and Cryptocurrency, to the competition. Everyone in the competition will have access to this.

4. Goal. The goal is simple – trade your account for the whole duration of the competition period and aim for the highest profits. The participants with the highest rankings while playing within the rules will be recognized as winners.

5. Multi Asset Portfolio. Each participant will have three (3) portfolios, one for each market (PSE, Crypto, and US) with 100,000 in buying power each.

PSE Portfolio

US Portfolio

Crypto Portfolio

₱ 100,000

$ 100,000

$100,000

You may opt to only trade one market, but this will put you at a disadvantage. So, it’s best that you take advantage of opportunities in all three markets.

6. Trading Hours.

PSE Trading Hours – 9:30am to 3:00pm

US Market Trading Hours (in PH Time) – 10:30pm to 4:30am

Cryptocurrency Trading Hours – 24 hours

7. Tradable Asset List. Participants can only trade the listed tradable assets for this competition. The tradable assets are filtered by our system and qualify as liquid and actively traded assets. You will be able to access the whole asset list once you are added to the Competition Room. This will be announced two weeks before the competition starts.

8. Diversification. To promote diversification and risk management, maximum exposure in a single asset can only be 1/3 or 33.33% of the portfolio. This requires the participants to buy at least 3 different assets should they want to fully invest their portfolio. The system won’t allow you to allocate more than 33.33% in a single stock.

The 33.33% rule applies to all portfolios. (PSE, US, and Crypto)

9. Trader Milestone. Participants can now receive rewards during competition by hitting certain milestones in their Trading Cup journey. Milestone rewards include:

Exclusive Trading Cup 2024 profile badges

Limited edition Investa Merchandise (for distribution after the competition ends)

InvestaGems

Exclusive Trading Cup Defense recording access

To claim the Milestones:

The collective profit across all three portfolios must reach the specified percentage.

Profit checking (for milestone unlocks) happens once a day only after the Philippine Stock Exchange (PSE) closes, not in real time.

10. Transaction Trading Fees (Long and Short Positions). To simulate real-life trading transaction fees on trading will apply with the following fee structure:

Market

Transaction Fees(long and short)

PSE

Approximately at 1.20% transaction fees (following PSE Standard comms, fees & vat on online trading)

US

0.25% per transaction

CRYPTO

0.10% per transaction

11. Buying and Selling Conditions (For LONG positions). Participants now have two options when transacting.

OPTION 1: The first option for transaction in this trading competition is to utilize limit orders for buying and selling specific assets. Instead of transacting at the current market price as with market orders, participants will set their own desired purchase or sale price through limit orders. This method ensures that trades are executed only when the stock price reaches the predetermined level set by the trader, offering more control over the transaction price.

It’s important to note that while limit orders provide price certainty, they do not guarantee execution, as the market may never hit the specified price. This approach is ideal for participants who prefer strategic entry and exit points, and are willing to wait for their target prices.

OPTION 2: The second option is to transact using our CONDITIONAL ORDERS. By using Conditional Orders, you won’t need to watch the market the whole day in order to transact in the market, you can now set AUTO CUT LOSS, AUTO TAKE PROFIT, and AUTO BUY ON BREAKOUT.

All these orders are by default GOOD TILL CANCELED, the order will remain active until your buy/sell price is hit or until the order is canceled . Watch this tutorial.

Buy – You can buy the same asset multiple times within a day.

Sell – YOU CAN SELL THE SAME ASSET SIX (6) TIMES PER DAY.

In one asset per day you can sell TWO TIMES (2) at a PROFIT.

In one asset per day you can sell FOUR TIMES (4) at a LOSS. (cutloss)

12. Buying and Selling Conditions (For SHORT positions). SHORTING is now available for this competition. The same thing applies if you want to short an asset, you can transact using the current price or set conditional orders if you can’t keep an eye on the market. We understand that many may not know the concept of shorting which is why we created a video tutorial you can watch here: LINK TO VIDEO

Sell – You can open a short position on the same asset multiple times within a day.

Buy – YOU CAN COVER YOUR SHORT POSITION ON THE SAME ASSET SIX (6) TIMES PER DAY.In one asset per day you can cover your short position TWO TIMES (2) at a PROFIT. In one asset per day you can cover your short position FOUR TIMES (4) at a LOSS. (cutloss)

FEES / COMMISSIONS: Same as long positions in the specific market.

COMPUTATION OF PROFITS: (Sell price – cover price)*shares – fees

For those who are not familiar on how to trade SHORT POSITIONS, here’s a STEP-BY-STEP guide to short-selling assets for this competition:

1. Choose your position from the market order type (long or short).

2. Upon choosing the short position, input the initial number of shares you want to sell.

Note: To short an asset, you have to SELL it first. Then to cover your position, you will need to BUY the shares back. To learn more please watch the tutorial: LINK

3. For closing the short position, select the short option in the market order type and input the number of shares you want to buy to close your short position.

Holding period for all assets (For both LONG and SHORT positions).

We will be applying the twenty (20) minute time lock for taking profits to ALL ASSETS to avoid widespread and rinse-repeat trades.

There will be no time lock or restrictions when selling at a loss.

13. Revision of Tradable Assets. Investagrams has the right to remove any assets from the list should it suddenly become too illiquid, abusable and/or delisted. Furthermore, Investagrams may also add new assets on the tradable list as new assets become more active and tradable in the market. All changes will be announced via the InvestaGroup and the Facebook Group upon revision of tradable assets.

In such cases that an asset is to be removed, we will follow this process:

Investagrams shall notify all the participants via the Investagrams Platform through an automated notification blast if there are any changes in the tradable assets list.

If you still have the asset in your portfolio, you can sell it at any point in time at your discretion.

Note: It is the participants responsibility to stay updated on the tradable assets list.

14. Initial Public Offering (IPO). All upcoming IPOs (in the PSE) that will happen while the Investagrams Trading Cup 2024 is on-going will be added on its SECOND (2nd) trading day.

15. On Dividends that will be given during the Trading Cup 2024.

Stock Dividends that will be released by a company will be credited at the END OF THE DAY of the ex-date. Please note that stock dividends will cause price adjustments, so be aware if a stock you’re holding will release stock dividends.

Cash Dividends that will be released by a company will NOT be credited to your total equity as the current system is still not able to credit cash divs.

Dividends whether stock or cash divs are only applicable to PSE.

16. On SRO that may happen during the Trading Cup 2024.

Stock Rights Offerings (or SRO) is offered to existing shareholders of a specific stock to purchase additional shares at a price lower than the current market price in addition to their current shares at hand.

SRO’s can be deemed good for longer-term investors. However, in the short term, may POTENTIALLY lead to a possible decline or gap down in the stock. So it’s important to always be aware of this.

Participants in the Trading Cup 2024 will not have an option to purchase additional shares from the SRO.

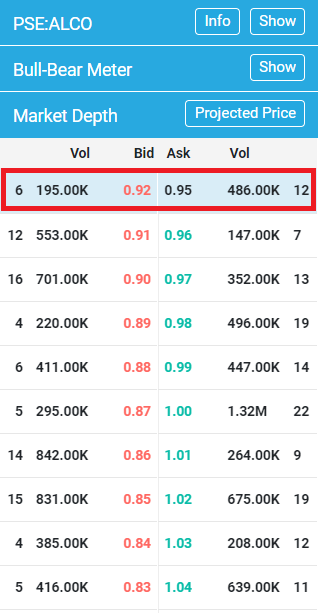

17. For stocks in the PSE that will be detected by our WIDE-SPREAD DETECTION SYSTEM (WSDS). The Wide-Spread Detection System’s main condition is that the first (1st) best bid and ask should never be more than 2% at any moment during open market session. This is only applicable in the PSE.

Fig 1. Real-time Market Depth / Orderbook showing the first (1st) best bid-ask data.

Example: $ATN (Refer to Fig. 1)

Given:

1st best bid = 1.11

1st best ask = 1.14

Formula:

X = (1st best ask – 1st best bid) / 1st best bid

Condition:

If X is greater than 2% then WSDS detects that the stock is wide-spread and can be abused.

Solution:

X = (1.14 – 1.11) / 1.11 = 0.02700 x 100% = 2.70%

Verdict:

Since X is greater than 2% then the stock is wide-spread as computed by the system.

The participant will be given a prompt that the detected stock is not tradable upon executing a buy or sell transaction.

The stock will again be tradable once the system detects that the spread of the 1st best bids/asks are below 2%.

18. On Trading Abuses.

Day trading opportunities on natural market moves are normal, but please take note that Investagrams will be on full-guard against participants that abuse illiquid opportunities. We want our winners to show real trading skills that are applicable in the PSE and Global Markets. Abuse of intraday spread trades will NOT BE TOLERATED. These rules are set to protect against the usual ‘rinse-and-repeat’ abuses that are mostly used in virtual trading competitions like this.

Any participants that have more than 10% of their profits from rinse-and-repeat wide spread, illiquid and other abusive trades will be penalized or DISQUALIFIED. We will be able to validate this through our data and algorithms that verify the historical transactions of each participant.

Any form of hacks, cheats, and abuses shall not be tolerated and will have corresponding repercussions. Suspicious behavior that may not be specified in the rules may also be flagged as ‘abusive’ trading behavior. All trade records shall be verified and those who fail to follow the rules will be disqualified.

Any participant who has constantly repeated any abusive trading behaviors (whether illiquid stocks, system abuses, loophole abuses) will instantly be DISQUALIFIED. Investagrams has the right to review any suspicious activity, and if the behavior is deemed inconsistent with real life trading then the said participant shall be disqualified.

A warning may be given, however, if the total profits of a participant have already reached 10% from rinse and repeat abuses upon initial review, an automatic disqualification will happen with no warning.

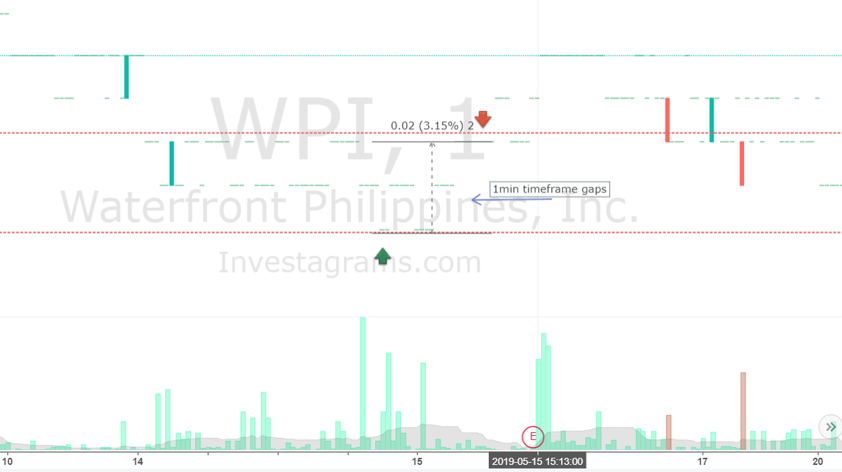

Questionable Transactions. Questionable transactions will be cross-checked through the buy and sell transaction time and the traded stock. Assets that have more than 2% consistent gaps in the one (1) minute timeframe within the transaction period shall be deemed invalid and Investagrams has the right to deduct the profits from the said transactions. It is normal to trade natural intraday moves and gaps can really happen, but if a participant is constantly trading assets that have gaps within one (1) minute timeframe and their profits from these kinds of scenarios make up more than 10% of their total profits, then he/she will be automatically disqualified.

Fig 2. Example 1 for one (1) minute time frame gaps with buy (green arrow) and sell (red arrow) transactions

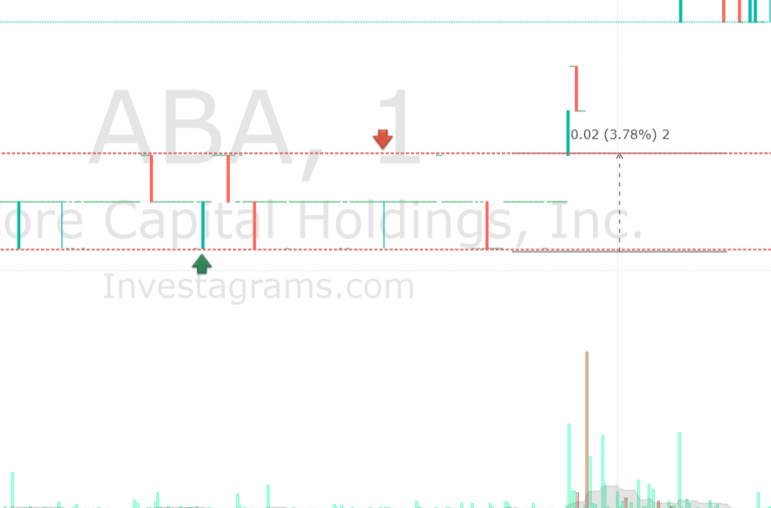

Fig 3. Example 2 for one (1) min. time frame abusable 2% gaps

Fig 4. Example 3 for one (1) min. time frame abusable 2% gaps

Investagrams will disqualify any participant that is proven to be constantly transacting with illiquid assets with 2% one (1) minute gaps. Basically, any asset that has 2% spreads and does not really have a trend is included in this definition. Any participant that is proven to repeat this kind of behavior shall be disqualified.

19. Trading halt. Stocks that are on a trading halt will not be tradable during the halt and will be tradable again during the announced lifting time.

20. Participant rankings. This is constantly updated every 10-minutes and automatically ranked by Investagrams system according to net profit gain/loss.

21. How winners will be identified. To identify our Top 40 winners for the Investagrams Trading Cup 2024, the percentage gain of all three portfolios will be taken into account. The Top 40 participants with the highest total % gain from all three portfolios will be selected as our winners.

22. Top 10 Winners. Those who make it to the Top 10 will be REQUIRED to do a defense of their trading strategies used during the competition. This is basically a presentation where you will share your biggest winners, losses, and learnings during the Trading Cup. This has been the tradition of the Trading Cup for the past few years where the winners will share with the community how they made it to the top.

NO DEFENSE = NO CASH PRIZE.

23. Unexpected events. In the case of an unexpected event that interrupts the operations of PSE or the system of Investagrams, the competition shall be frozen and paused. Further notice shall be given and trading will resume once everything is back to normal.

24. Modification and adding of rules. Investagrams has the right to modify the rules of the competition and add protective measures against any future abuses that may arise to ensure the integrity of the Investagrams Trading Cup 2024: The Global Quest. Announcements shall be made if there are any changes. Rest assured, we prioritize keeping the competition as FAIR as possible to all participants.

25. Ignorance of the rules is no excuse. All participants are expected to have read and understood the rules and mechanics of Investagrams Trading Cup 2024: The Global Quest. These are published for the participants’ information and protection. Ignorance of these rules and mechanics is not an acceptable excuse for violation.

26. If you are part of the Top 40 winners, the FINAL DEADLINE to claim your cash prize is on August 31, 2024. The cash prize will not be given anymore past this date.

27. Sponsors. Apple is not involved in any way in this competition. The sponsor(s) is/are solely responsible for providing the prize(s) listed herein. The prize(s) won are not apple products, nor are they related to apple in any way. The responsibility of organizing this competition and distributing the prize(s) are the sponsors’ responsibilities. Apple does not sponsor this competition in any way.

28. Prizes from Partners. Some of our partners will be giving out prizes (in cash or in kind) which may be distributed on a different timeline or date depending on the partner. But rest assured that we will make sure that they will be provided.

29. Ultimate Pioneers. The Ultimate Pioneers will get free access to the competition and the trading cup defense. A special email will be sent to all Ultimate Pioneers to claim your free slot to the competition. You will have until March 31, 2024 to confirm your participation.

30. Joining theInvestagrams Trading Cup 2024: The Global Quest means that you agree with all the clauses mentioned above.

Investing is the process of putting your money to work for you, with the expectation of earning a return over time. Investing can help you achieve your financial goals, such as saving for retirement, buying a house, or funding your education. Investing can also help you grow your wealth, beat inflation, and create passive income.

However, investing is not a get-rich-quick scheme, nor a gamble. Investing requires patience, discipline, and a long-term perspective. Patience is crucial for investing, as it can help you overcome the challenges and uncertainties of the market, and reap the rewards of compounding and diversification. In this article, we will discuss some of the reasons why it is crucial for investing, and how to cultivate it.

Patience helps you ignore the noise

The market is full of noise, such as news, opinions, rumors, emotions, and events, that can influence your investing decisions. However, most of the noise is irrelevant, misleading, or short-term, and does not reflect the true value or potential of your investments. Patience helps you ignore the noise, and focus on the signal, such as the fundamentals, trends, and quality of your investments. It helps you avoid making impulsive, emotional, or irrational decisions, such as buying high, selling low, chasing fads, or following the crowd. Patience helps you stick to your investing plan, and act based on facts, logic, and analysis.

Patience helps you benefit from compounding interest

Compounding is the process of earning interest on your interest, or returns on your returns, over time. Compounding is one of the most powerful forces in investing, as it can exponentially increase your wealth, especially in the long run. However, compounding requires patience, as it takes time to accumulate and grow. Patience helps you reinvest your earnings, and let them compound over time. Patience helps you avoid withdrawing your money prematurely, or switching your investments frequently, which can reduce your compounding effect. Patience helps you harness the power of compounding, and achieve higher returns with lower risk.

Patience helps you diversify your portfolio

Diversification is the process of spreading your money across different types of investments, such as stocks, bonds, commodities, real estate, or cash, that have different characteristics, risks, and returns. Diversification is one of the most effective ways to reduce your portfolio risk, as it can protect you from the volatility and unpredictability of the market. However, diversification requires patience, as it means accepting lower returns in some periods, or holding some investments that may underperform or lose value. Patience helps you diversify your portfolio, and balance your risk and return. Patience helps you avoid putting all your eggs in one basket, or chasing the best-performing investments, which can expose you to more risk. Patience helps you optimize your portfolio performance, and achieve more consistent and stable returns.

How to Cultivate Patience for Investing

Set realistic and long-term goals: Patience for investing starts with setting realistic and long-term goals, such as saving for retirement, buying a house, or funding your education. You should have a clear and specific vision of what you want to achieve, why you want to achieve it, and how you plan to achieve it. You should also have a realistic and reasonable expectation of the returns and risks of your investments, and how long it will take to reach your goals. Setting realistic and long-term goals can help you stay motivated and committed, and avoid disappointment and frustration.

Do your research and due diligence: Patience for investing also requires doing your research and due diligence, such as studying the market, analyzing the investments, and evaluating the opportunities. You should have a sound and rational basis for your investing decisions, and not rely on hearsay, hype, or speculation. You should also have a thorough and objective understanding of the strengths, weaknesses, opportunities, and threats of your investments, and how they fit your goals, risk tolerance, and time horizon. Doing your research and due diligence can help you build your confidence and conviction, and avoid doubt and fear.

Review and monitor your progress: Patience for investing also involves reviewing and monitoring your progress, such as tracking your portfolio performance, measuring your results, and adjusting your strategy. You should have a regular and consistent schedule for reviewing and monitoring your progress, such as monthly, quarterly, or annually, and not too frequently or infrequently. You should also have a clear and relevant benchmark for comparing and evaluating your progress, such as an index, a peer group, or your own goals. Reviewing and monitoring your progress can help you learn from your successes and failures, and improve your decision making.

Conclusion

Patience is crucial for investing, as it can help you overcome the challenges and uncertainties of the market, and reap the rewards of compounding and diversification. Patience can help you ignore the noise, benefit from compounding, and diversify your portfolio. Patience can also help you set realistic and long-term goals, do your research and due diligence, and review and monitor your progress.

Patience is not easy, nor natural, for most investors, as it goes against the human nature of wanting instant gratification or avoiding pain and loss. However, patience can be cultivated, practiced, and improved, with the right mindset, attitude, and habits. Patience can make the difference between success and failure, wealth and poverty, happiness and misery, in investing and in life.

On Wednesday, January 10, 2024, the U.S. Securities and Exchange Commission (SEC) approved 11 applications for spot bitcoin ETFs, clearing the way for them to start trading on Thursday, January 11, 2024. This is a historic moment for the crypto industry, as it marks the first time that the SEC has allowed investors to access bitcoin directly through a regulated and transparent vehicle.

How It Happened

The approval of spot bitcoin ETFs has been a long-awaited and highly anticipated event for the crypto community. The first application for a bitcoin ETF was filed by the Winklevoss twins in 2013. However, the SEC rejected it in 2017. They cited concerns over market manipulation, fraud, and lack of regulation. Since then, many other applications have been submitted but none have received the green light until now.

The tide began to turn in 2021, when the SEC approved several bitcoin ETFs based on futures contracts, which are derivatives that track the price of bitcoin without holding the actual asset. These products, however, have higher fees, lower liquidity, and more complexity than spot bitcoin ETFs, which directly hold bitcoin in custody and reflect its market price.

The breakthrough came in June 2023, when Blackrock, the world’s largest asset manager, filed an application for a spot bitcoin ETF, signaling its confidence in the crypto space and its readiness to meet the SEC’s standards. Following Blackrock’s move, many other prominent financial firms, such as Fidelity, VanEck, WisdomTree, and Invesco, also filed their own applications for spot bitcoin ETFs, creating a critical mass of support and pressure for the SEC to act.

The SEC finally announced its approval of 11 spot bitcoin ETFs on Wednesday, January 10, 2024, after the close of trading. The approved products are:

Blackrock’s iShares Bitcoin Trust (IBIT)

ARK 21Shares Bitcoin ETF (ARKB)

WisdomTree Bitcoin Fund (BTCW)

Invesco Galaxy Bitcoin ETF (BTCO)

Bitwise Bitcoin ETF (BITB)

VanEck Bitcoin Trust (HODL)

Franklin Bitcoin ETF (EZBC)

Fidelity Wise Origin Bitcoin Trust (FBTC)

Valkyrie Bitcoin Fund (BRRR)

Grayscale Bitcoin Trust (GBTC)

Hashdex Bitcoin ETF (DEFI)

These products will be listed and traded on various stock exchanges such as Cboe, NYSE, and Nasdaq. Trading of BTC ETFs will start on Thursday, January 11, 2024.

What It Means for the Market

The approval of spot bitcoin ETFs is expected to have a positive impact on the crypto market. It will make bitcoin more accessible, attractive, and mainstream for investors. Some of the potential benefits are:

Increased demand and adoption

Spot bitcoin ETFs will lower the barriers to entry and reduce the friction for investors. This is especially true for institutional and retail investors who prefer to use traditional and regulated platforms. Spot bitcoin ETFs will also increase the visibility and awareness of bitcoin among the general public.

Improved liquidity and efficiency

Spot bitcoin ETFs will increase the trading volume and liquidity of bitcoin, as they will create more arbitrage opportunities and market participants. They will also improve the price discovery and efficiency of bitcoin. Hopefully, this will reflect its true market value and reduce the discrepancies between different platforms and regions.

Enhanced security and transparency

Spot bitcoin ETFs will offer a higher level of security and transparency for investors. they will be subject to the oversight and regulation of the SEC and other authorities. Spot bitcoin ETFs will also have to comply with strict standards of custody, auditing, reporting, and disclosure. This is all to ensure that investors’ funds are safe and accounted for.

On a Side Note

The approval of spot bitcoin ETFs is a major milestone for the crypto industry, as it demonstrates the growing recognition and acceptance of bitcoin as a legitimate and valuable asset class. Spot bitcoin ETFs will likely boost the adoption and innovation of bitcoin and other cryptocurrencies, paving the way for a more inclusive and decentralized financial system.

While this is definitely a bullish development, remember that anything can happen in the markets. Cryptocurrencies will most likely experience long-lasting bullishness. However, this news could become a “sell on news” kind of event given that everyone has already been anticipating this to occur.